Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

QUARTERLY REPORTS Q1 2023

We are seeing signs of price stabilization and some growth after the market correction of 2022! Illustrated on the front is the up-down-up trajectory that home prices have experienced over the last year. While we are in the midst of measuring the negative difference from the peak prices of the first half of 2022 to now, we are still up 12 months over 12 months, and most recently prices are up from last month.

The correction in prices was a result of a 3-point increase in interest rates over the second half of 2022. Data shows the market has recalibrated in 2023 which has increased buyer demand as consumers have become more comfortable with the “new normal”. This has caused prices to stabilize and start to grow month-over-month since January. Days on market are shrinking and sale prices are averaging closer to the list prices, and in some cases are escalating over the list price. It has been an eventful past year highlighting the importance of real-time, accurate information to help empower strong decisions. Moves are motivated by life changes, lifestyle goals, and strategic financial planning. If you or someone you know is curious about how the market relates to these needs, please reach out.

Housing Absorption Trends, Interest Rates Hovering, and Inventory Constricting.

Three key elements to pay attention to when assessing prices and the real estate market.

As we round out the first quarter of 2023, three real-time trends to pay close attention to in order to truly understand what is happening in the real estate market are absorption data, interest rates, and inventory levels. Right now, we are in the midst of the market heating up due to seasonality, pent-up buyer demand, and rates finding their new normal. The media will often lag in reporting the latest information (pending sale data) and will latch onto closed sale data, which is outdated. I am here to keep you on the frontline of market activity so you are connected to the most current data to keep you well informed.

As we round out the first quarter of 2023, three real-time trends to pay close attention to in order to truly understand what is happening in the real estate market are absorption data, interest rates, and inventory levels. Right now, we are in the midst of the market heating up due to seasonality, pent-up buyer demand, and rates finding their new normal. The media will often lag in reporting the latest information (pending sale data) and will latch onto closed sale data, which is outdated. I am here to keep you on the frontline of market activity so you are connected to the most current data to keep you well informed.

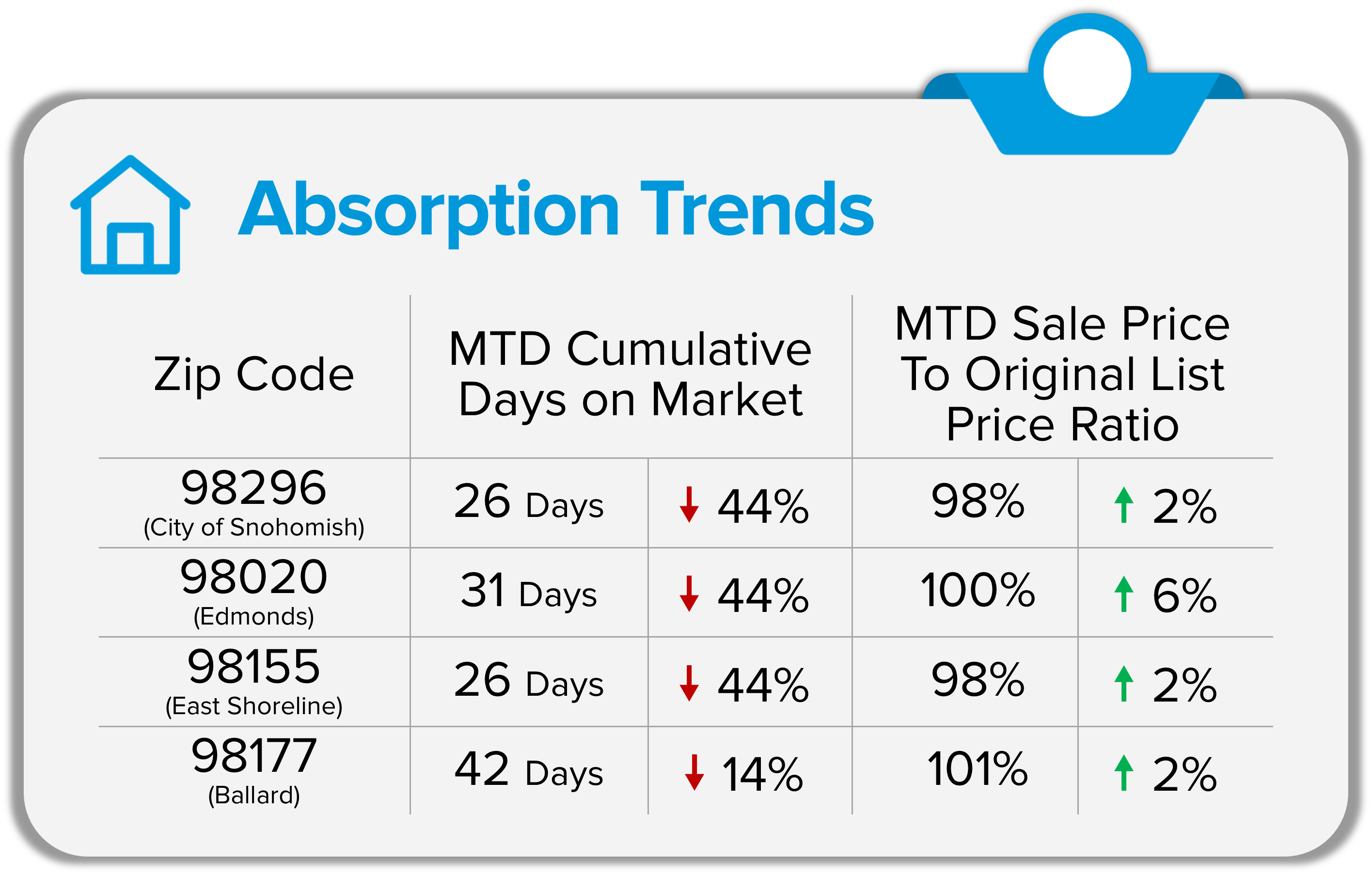

Let’s start with absorption data. Month-to-date (3/1/23-3/27/23), days on market are shrinking and sale price to original list price ratios are climbing. This means that houses are selling faster and negotiations are becoming more competitive for buyers. I was able to determine that these trends are fluid from Snohomish County to King County by analyzing four zip codes: 98296 (City of Snohomish), 98020 (Edmonds), 98155 (East Shoreline), 98117 (Ballard).

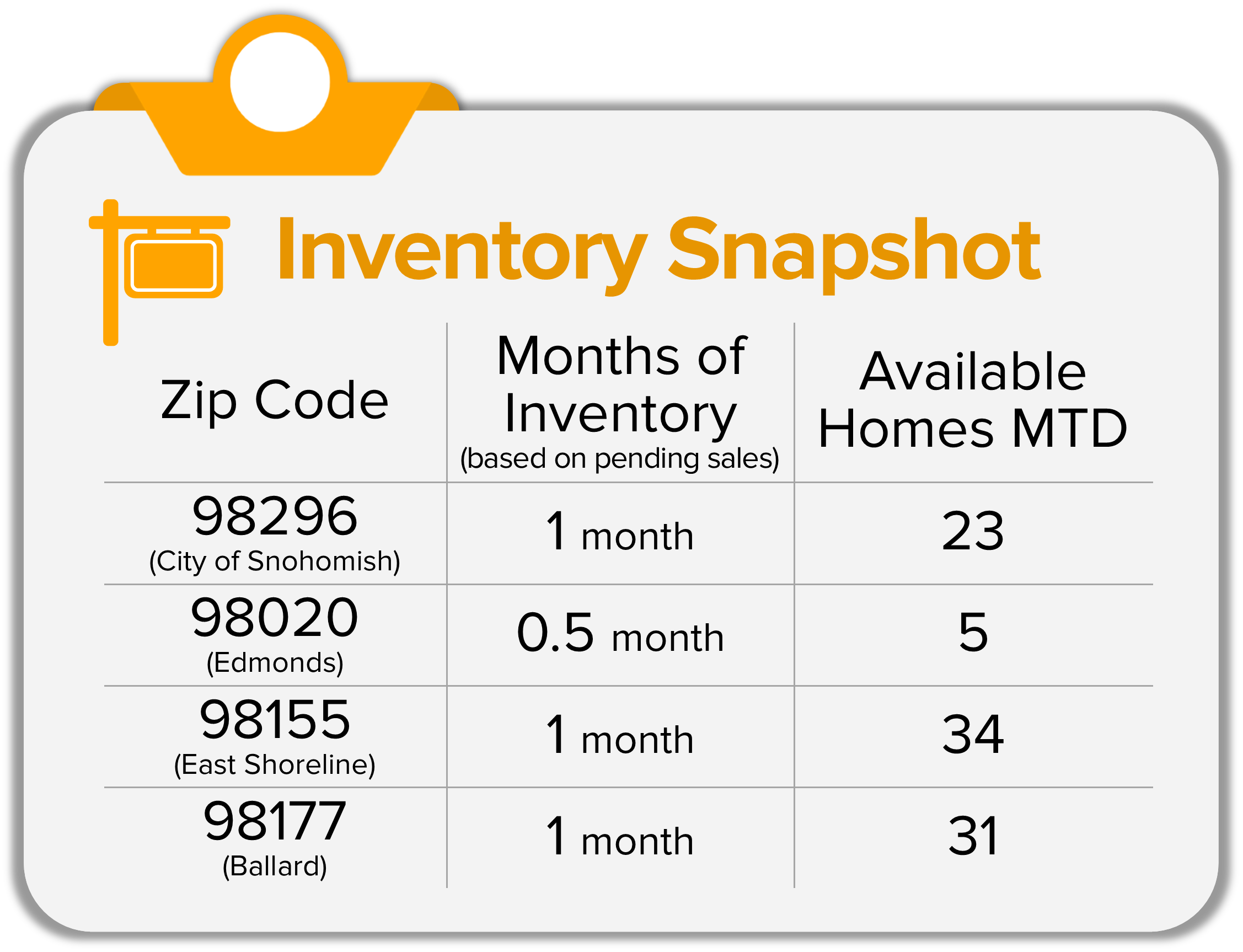

Available inventory is constricting due to an increase in absorption and new listings lagging. As we head into spring, we will see a seasonal uptick in new listings which will be welcomed by a healthy buyer audience. Month-to-date, inventory levels based on pending sales show a seller’s market (0-2 months). You calculate months of inventory by taking the number of available homes and dividing it by the number of pending sales. If no new homes came to market the trend suggests we would sell out of homes in this amount of time. Month-to-date the actual number of homes available in each zip code is quite limited and a welcome sign for more new listings as we head into Spring. Again, I pulled the data for the four zip codes to represent a sampling of both Snohomish and King Counties.

Available inventory is constricting due to an increase in absorption and new listings lagging. As we head into spring, we will see a seasonal uptick in new listings which will be welcomed by a healthy buyer audience. Month-to-date, inventory levels based on pending sales show a seller’s market (0-2 months). You calculate months of inventory by taking the number of available homes and dividing it by the number of pending sales. If no new homes came to market the trend suggests we would sell out of homes in this amount of time. Month-to-date the actual number of homes available in each zip code is quite limited and a welcome sign for more new listings as we head into Spring. Again, I pulled the data for the four zip codes to represent a sampling of both Snohomish and King Counties.

Both of the trends above have been determined by buyers becoming more comfortable with the new normal of interest rates. The correction in the market that we experienced in 2022 was a result of a 3-point increase in interest rates. After prices adjusted to levels that would work with the higher rates, buyers started to return to the market. 2-3% and maybe even 4% interest rates will be folklore we tell our grandchildren about. People that want to make a move have come to terms with adapting to the higher rates and making these important life transitions. Today’s rates are much more in line with the average over the last 30 years.

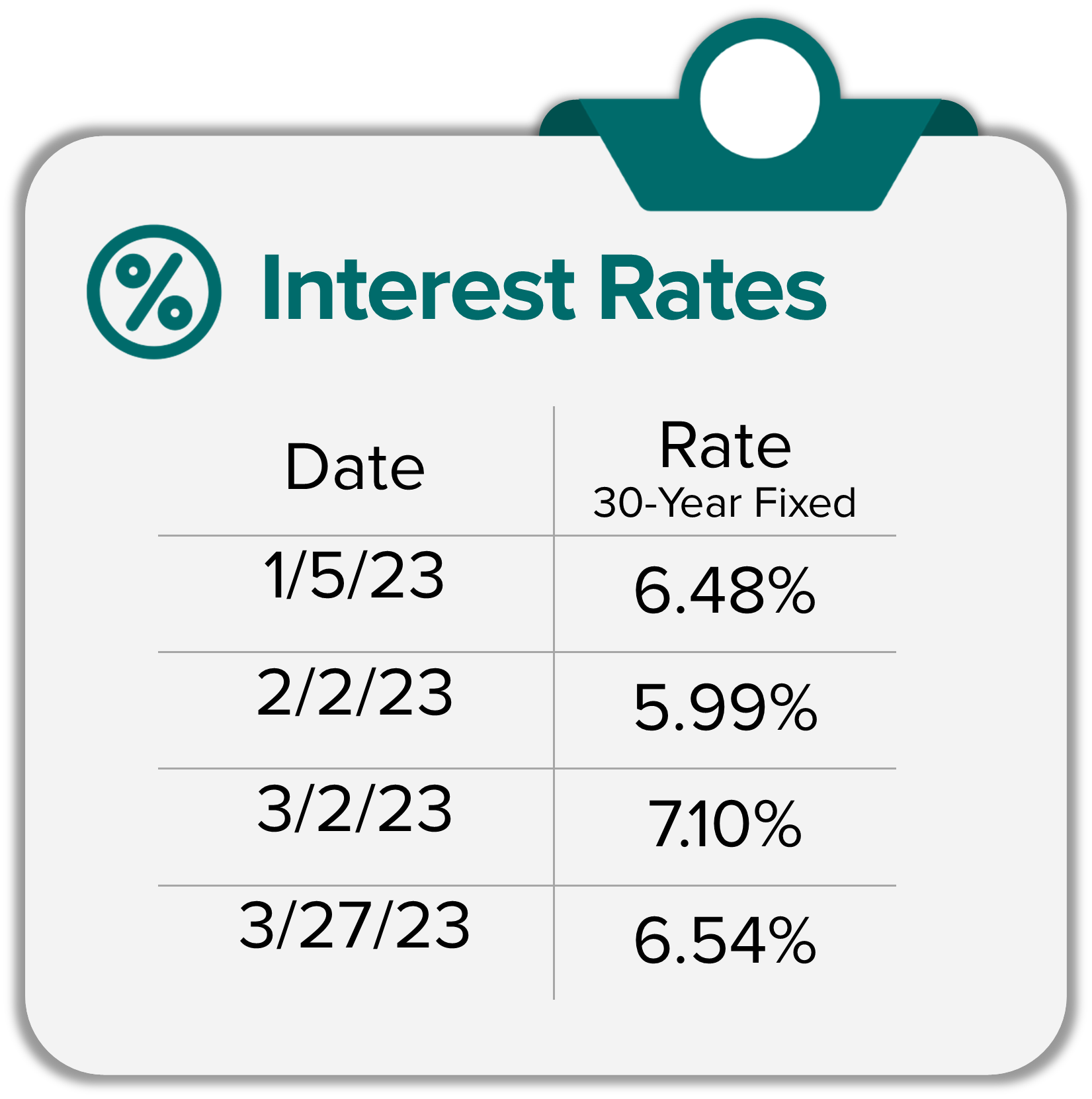

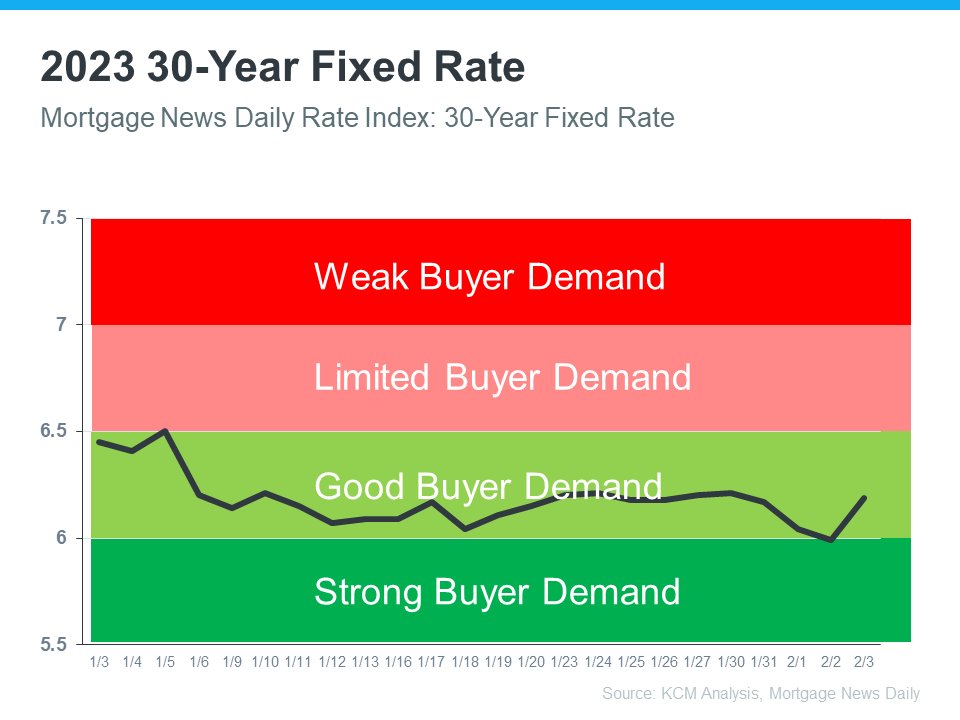

At the start of 2023, the 30-year fixed mortgage was at 6.48%, then dropped to 5.99% in early February, peaked at 7.1% in early March, and is now back down to 6.54% at press time. Rates have been volatile as the Fed tries to manage inflation. You can access a video below from Matthew Gardner explaining the effect of the Fed and the recent bank failures on interest rates and the real estate market overall.

At the start of 2023, the 30-year fixed mortgage was at 6.48%, then dropped to 5.99% in early February, peaked at 7.1% in early March, and is now back down to 6.54% at press time. Rates have been volatile as the Fed tries to manage inflation. You can access a video below from Matthew Gardner explaining the effect of the Fed and the recent bank failures on interest rates and the real estate market overall.

One item to note is that mortgage rates are long-term interest rates, and when you hear about the Fed raising rates they are referring to short-term rates such as car loans, credit cards, and home equity loans. The media does not make that distinction, often confusing the public. In fact, in some cases when the short-term rate has been increased, we have seen mortgage rates drop. Here is a great website to follow to get a real-time read on rates.

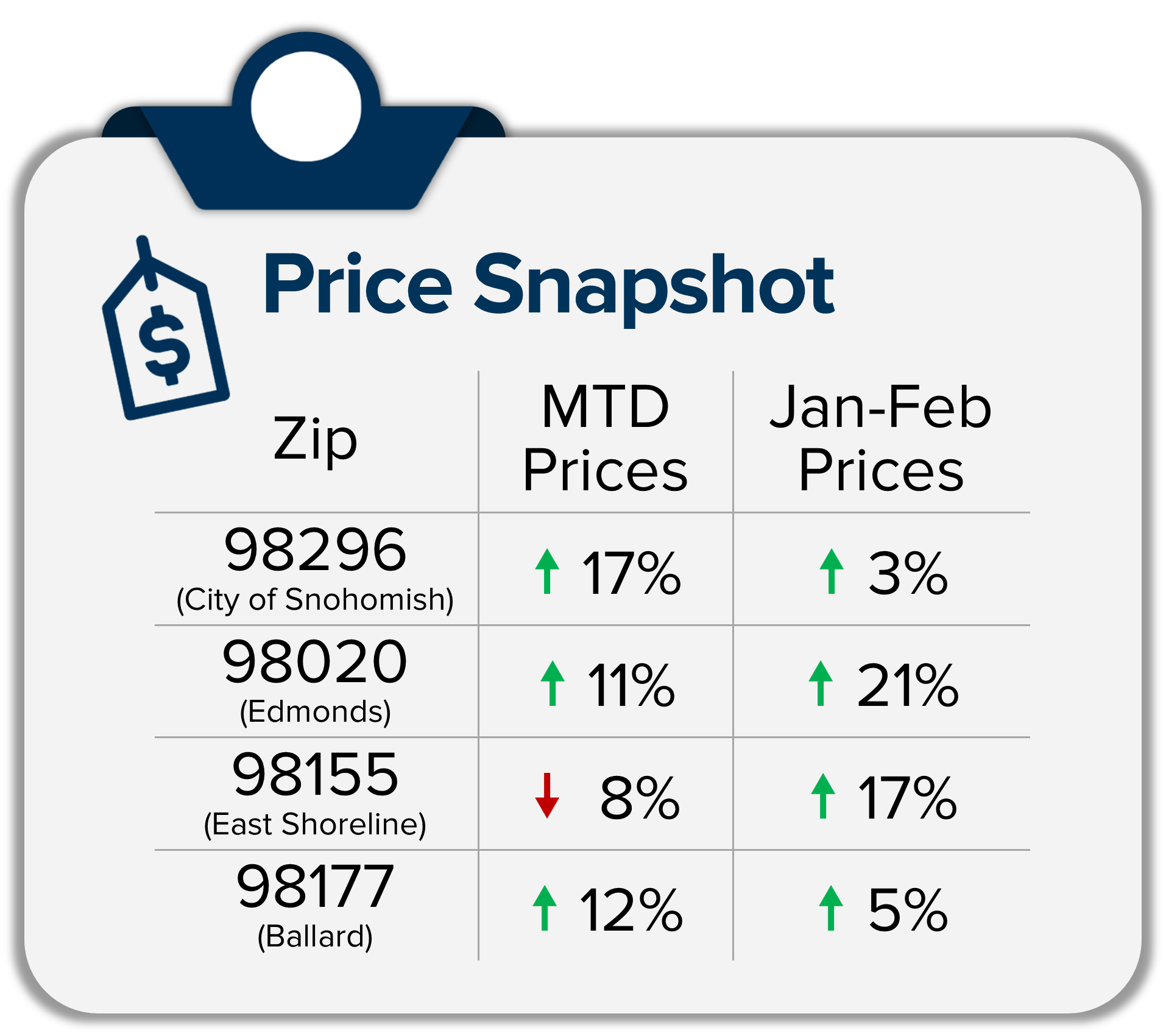

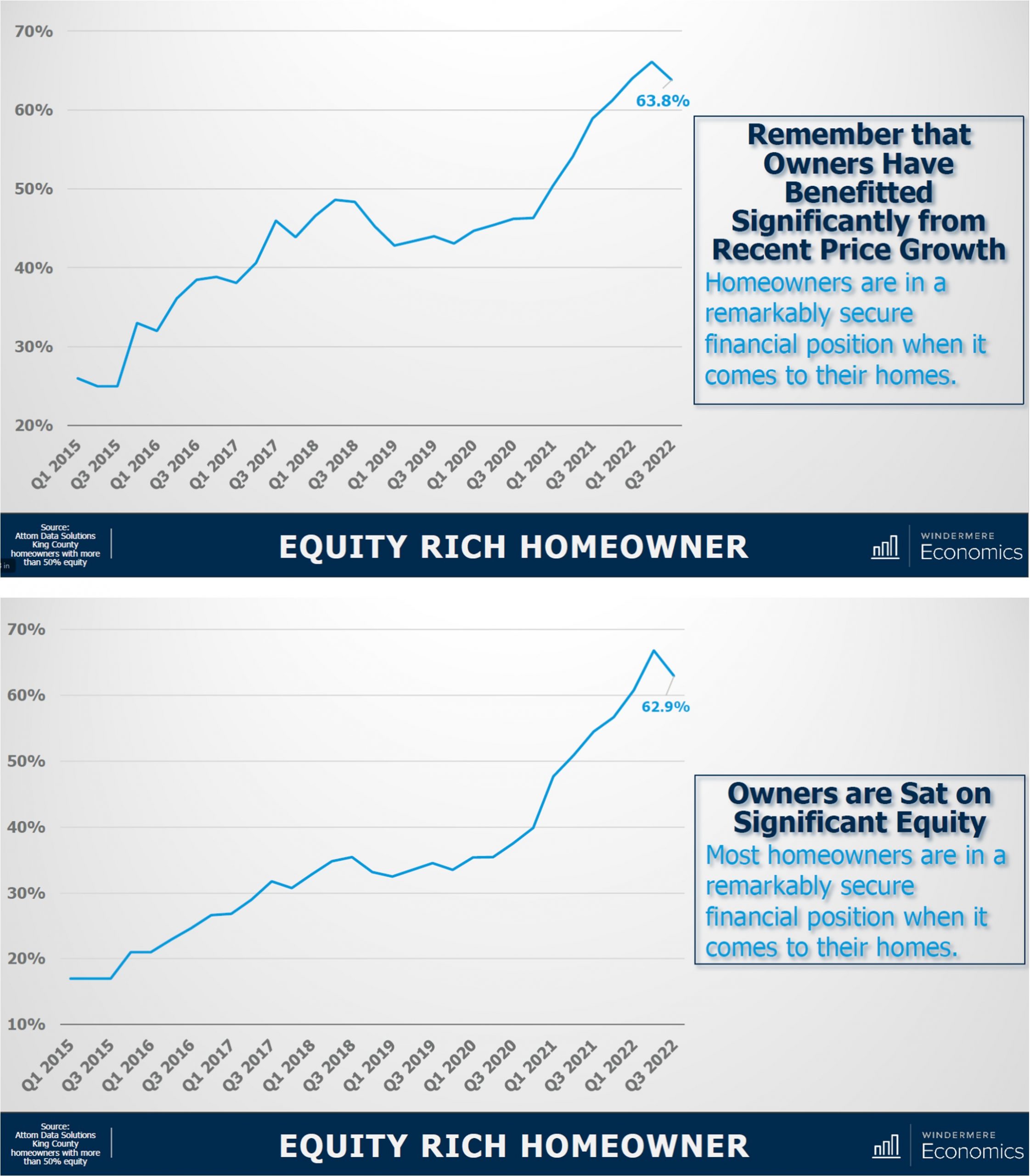

Interest rates finding their way, the psychological acceptance of the new normal, and people needing to make moves to adapt to their life changes have led to prices starting to stabilize and even grow in some markets. I pulled the month-to-date median price data for the four zip codes and it appears prices are leveling and growth is happening or will be in the near future. Bear in mind, that the bottom often comes in the form of a bounce before there is a consistent straight shot up. All signs are pointing to recovery from the correction in these areas noted. This growth will be added to the immense long-term price gains we have seen. Currently, 93% of all homeowners in the U.S. have positive home equity and 48% of homeowners have more than 50% equity.

During this time of change, it is important that each neighborhood and price point is researched individually. From the four zip code breakdowns above, it is clear that the trends vary. When I am asked the question, “How’s the Market?”, I am always curious to know what you have heard and what you want to learn about. Sweeping statements are dangerous and I am committed to diving into the data to educate my clients on how the trends affect their investments and their lifestyle.

During this time of change, it is important that each neighborhood and price point is researched individually. From the four zip code breakdowns above, it is clear that the trends vary. When I am asked the question, “How’s the Market?”, I am always curious to know what you have heard and what you want to learn about. Sweeping statements are dangerous and I am committed to diving into the data to educate my clients on how the trends affect their investments and their lifestyle.

With the market correction of 2022 in the rearview mirror and the recovering market of 2023 upon us it is important to understand that opportunity abounds. That opportunity is rooted in research. Solid research and discerning the data gathered help empower strong decisions and build trust. This is my process and my passion and it is all about helping people! If you are curious about how the latest trends match up with your investment and lifestyle goals, please reach out and we can dive in.

You’re invited to our annual Paper Shredding Event & Food Drive. We partner with Confidential Data Disposal to provide a safe, eco-friendly way to reduce your paper trail and help prevent identity theft.

Saturday, April 15th, 10AM to 2PM*

4211 Alderwood Mall Blvd, Lynnwood

Bring your sensitive documents to be professionally destroyed on-site. Limit 10 file boxes per visitor.

This is a paper-only event. No x-rays, electronics, recyclables, or any other materials.

We will also be collecting non-perishable food and cash donations to benefit Volunteers of America Western Washington food banks. Donations are not required, but are appreciated. Hope to see you there!

*Or until the trucks are full

Which is better, renting or buying? The financial benefits of owning real estate.

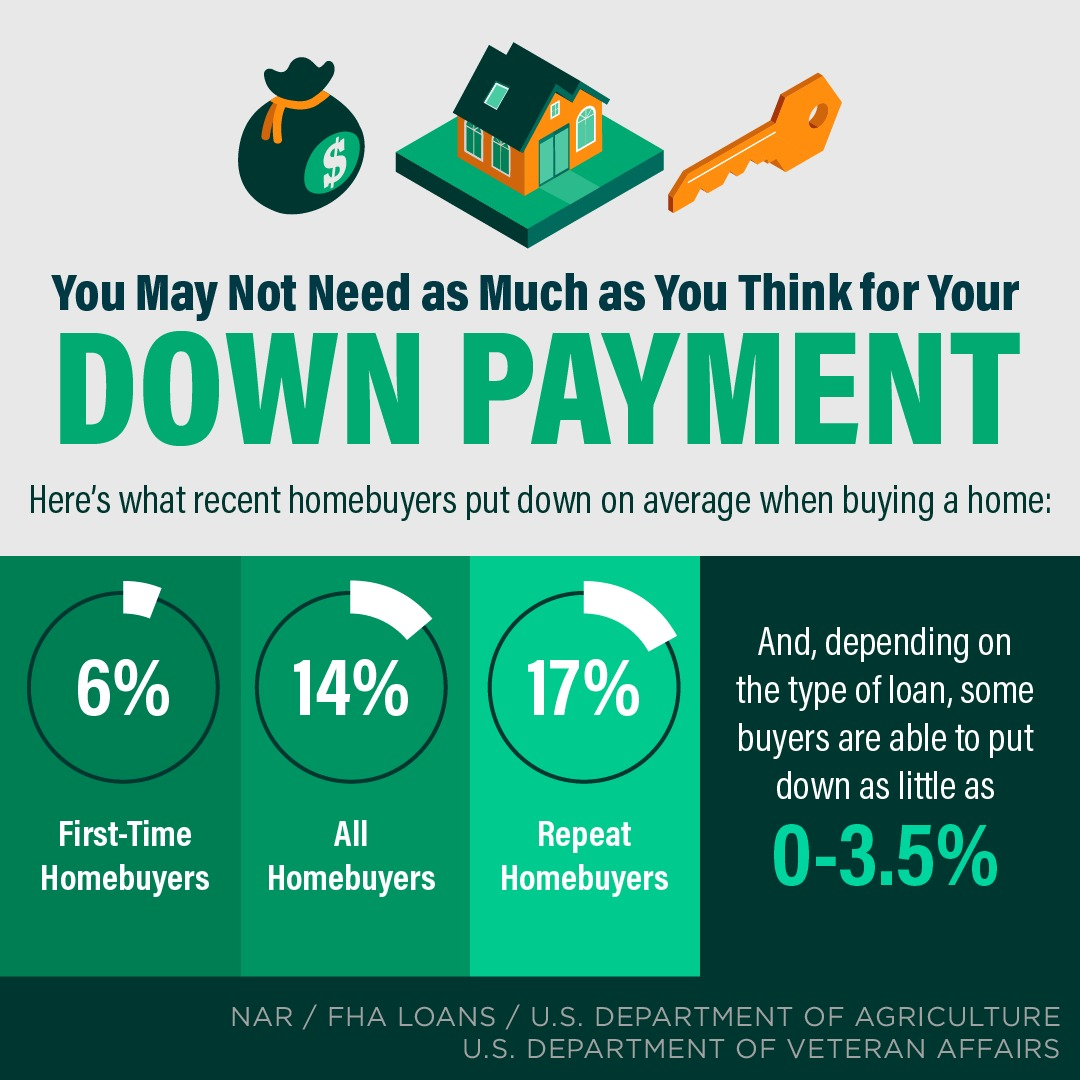

The financial benefits of owning real estate significantly outweigh the option of renting. Renting is certainly a must for some, and is what one may have to do while they build up to becoming a homeowner. Becoming a homeowner requires solid employment, good credit, and some type of down payment. Savings can all be built over time and if achieved can provide incredible long-term financial growth by becoming a down payment on a home. In fact, many people think you need a 20% down payment in order to purchase a home and that is just not the case. There are various loan programs available requiring much less than 20% down.

The financial benefits of owning real estate significantly outweigh the option of renting. Renting is certainly a must for some, and is what one may have to do while they build up to becoming a homeowner. Becoming a homeowner requires solid employment, good credit, and some type of down payment. Savings can all be built over time and if achieved can provide incredible long-term financial growth by becoming a down payment on a home. In fact, many people think you need a 20% down payment in order to purchase a home and that is just not the case. There are various loan programs available requiring much less than 20% down.

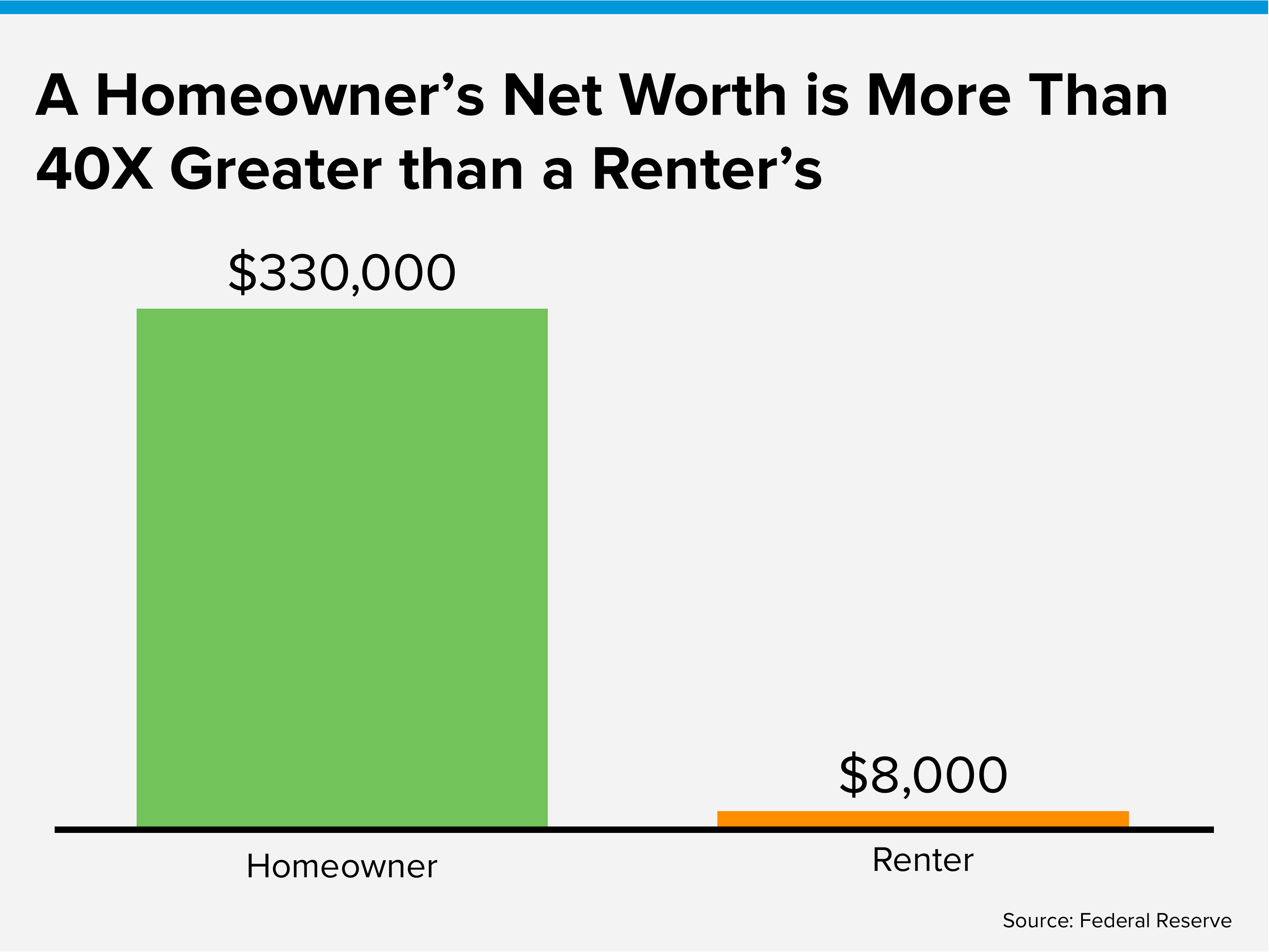

The savings of your nest egg that you would put into a home purchase is the single most powerful investment vehicle to build household wealth and financial security. Did you know that the average net worth of a homeowner is 40 times higher than one of a renter? There are many factors that play into this statistic. Take in my outline below as well as the video link below from Matthew Gardner, Windermere’s Chief Economist who also weighs in on this subject.

Over time, your mortgage payment becomes easier to afford. Fixed mortgage payments do not go up, but rent inevitably does. While your mortgage stays fixed your income often increases, making the monthly payment easier to handle.

Real estate is a solid long-term investment. Historical home price appreciation is on your side. The historical average is 3-5%, and in some cases, that figure has been much higher. Only once, during the Great Recession, did we see multiple-year price declines. However, the people that held onto those homes since that time have been handsomely rewarded with phenomenal equity. Real estate is a long-term hold investment that provides shelter and financial opportunity.

You cannot live in your stock certificate. Real estate is an investment that you can touch, feel, smell, live in, and improve! You have to live somewhere and allocate a portion of your income to shelter. Why not pay your shelter budget towards an asset that is growing for your financial future? You can also make improvements to your property that you can enjoy which will also increase the value of the asset. Diversifying your investments is important, stocks are a natural option, but real estate should be in the mix as well. I have even seen first-time buyers keep their starter home as a rental, move on to their next home and start to build their own real estate portfolio.

Every mortgage payment goes towards paying down your loan principle. Right now, mortgage rates are up a bit, leading to conversations about the impact of rates. One thing I know for sure is that the interest rate on rent is 100%! None of that money ever comes back to you. Your mortgage payment goes back into your asset and becomes a forced savings account. This piles your money safely away all while your asset is appreciating year-over-year which builds long-term wealth.

Owning real estate provides tax benefits. Depending on the state you live in, you can write off your real estate taxes and mortgage interest. This can offset your tax burden and save you significant money every year. There are also capital gains tax exemptions on your primary residence that you have lived in for at least two years of the last 5 years (make sure to consult your tax expert on the details). You can have tax-free gains of up to $250,000 for a single person and up to $500,000 for a married couple. This is a wonderful opportunity to move your wealth towards your future when planning for big lifestyle improvements such as retirement.

Owning real estate provides tax benefits. Depending on the state you live in, you can write off your real estate taxes and mortgage interest. This can offset your tax burden and save you significant money every year. There are also capital gains tax exemptions on your primary residence that you have lived in for at least two years of the last 5 years (make sure to consult your tax expert on the details). You can have tax-free gains of up to $250,000 for a single person and up to $500,000 for a married couple. This is a wonderful opportunity to move your wealth towards your future when planning for big lifestyle improvements such as retirement.

I will leave you with this: it can seem overwhelming to take on the task of buying your first home or to prepare to own again after renting. Start by understanding that shopping in the price range you can afford matters. Often times people want to get their forever home right off the bat and that makes the accomplishment of becoming a homeowner much harder. Figure out how much you can afford now and put your nest egg to work sooner rather than later to start building wealth. Maybe it is a small condo that fits your budget now, but over time the money saved and the equity built can turn into the down payment needed to purchase your forever home.

Owning real estate is a step-by-step journey that takes time and sacrifice. Your patience and commitment will be rewarded with compounded savings which will lead to building long-term wealth. It also creates a fond memory lane of that first condo or small house that you loved making a home, which then became the vehicle to afford the next home that better suited your lifestyle. If you are curious about the prospect of owning real estate or have a special person in your life who is poised to become a homeowner, please reach out. It is my goal to help people understand the process, align them with a trusted lender, help them make strong financial decisions, and match their living situation to their lifestyle.

You’re invited to our annual Paper Shredding Event & Food Drive. We partner with Confidential Data Disposal to provide a safe, eco-friendly way to reduce your paper trail and help prevent identity theft.

Saturday, April 15th, 10AM to 2PM*

4211 Alderwood Mall Blvd, Lynnwood

Bring your sensitive documents to be professionally destroyed on-site. Limit 10 file boxes per visitor.

This is a paper-only event. No x-rays, electronics, recyclables, or any other materials.

We will also be collecting non-perishable food and cash donations to benefit Volunteers of America Western Washington food banks. Donations are not required, but are appreciated. Hope to see you there!

*Or until the trucks are full

Holy Shift, Again! Most of the Market Correction Behind Us & Growth Ahead!

Markets change fast! We experienced a substantial shift in 2022 with the first half of the year feeling like a completely different market than the second half of the year. A 3-point increase in interest rate was the main culprit along with inflation and affordability for the 2022 market correction we experienced.

A market correction is defined by prices reverting by 10% or more. In January 2022 the median price in Snohomish County started at $700,000 then peaked at $830,000 in April, and ended the year at $689,000 (-17%). In King County, the median price started at $794,000 then peaked at $1,000,000 in May, and ended the year at $820,000 (-18%). Bear in mind that the December 2022 median price was also up 17% over the January 2021 median price in Snohomish County and up 12% in King County. This illustrates that the correction was only off the peak of spring 2022 not off of the strong equity that was built prior to that intense run-up.

A market correction is defined by prices reverting by 10% or more. In January 2022 the median price in Snohomish County started at $700,000 then peaked at $830,000 in April, and ended the year at $689,000 (-17%). In King County, the median price started at $794,000 then peaked at $1,000,000 in May, and ended the year at $820,000 (-18%). Bear in mind that the December 2022 median price was also up 17% over the January 2021 median price in Snohomish County and up 12% in King County. This illustrates that the correction was only off the peak of spring 2022 not off of the strong equity that was built prior to that intense run-up.

As we find ourselves in mid-Q1 2023 all data points and anecdotal stories are pointing to the worst of the market correction being behind us and yet again, another shift. Interest rates peaked in November 2022 at just over 7% and have since come down. Experts are predicting rates to find themselves under 6% as we travel through the easing of inflation in 2023.

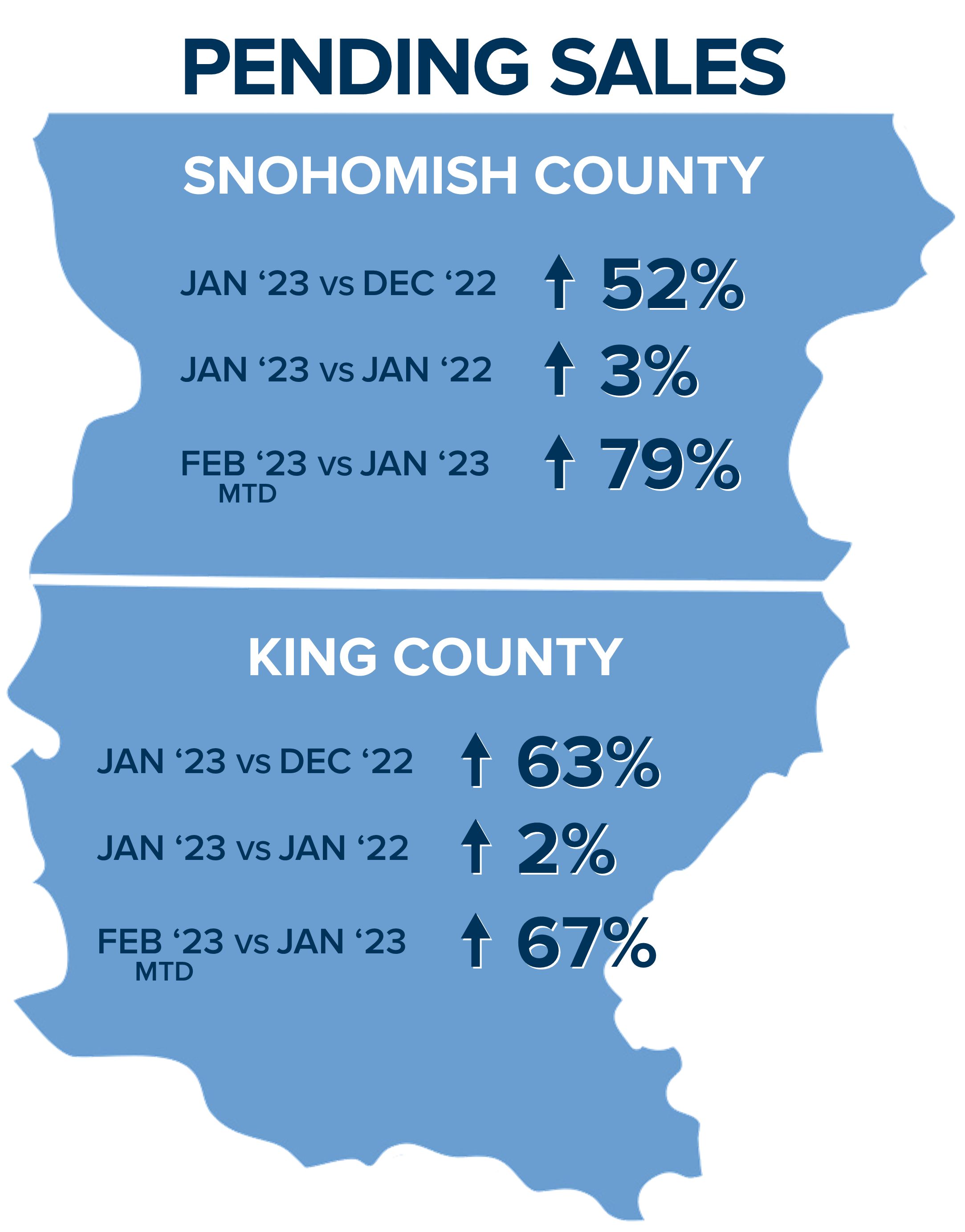

The well-defined price correction and interest rates lowering have brought many buyers back to the market. In fact, pending sales in Snohomish County in January 2023 were up 52% over December 2022 and were up 3% over January 2022. Even more so an indicator: pending sales are up 80% month-to-date (MTD) in February over January 2023! In King County, pending sales in January 2023 were up 63% over December 2022 and were up 2% over January 2022, and up 61% MTD over January 2023.

The well-defined price correction and interest rates lowering have brought many buyers back to the market. In fact, pending sales in Snohomish County in January 2023 were up 52% over December 2022 and were up 3% over January 2022. Even more so an indicator: pending sales are up 80% month-to-date (MTD) in February over January 2023! In King County, pending sales in January 2023 were up 63% over December 2022 and were up 2% over January 2022, and up 61% MTD over January 2023.

This pent-up demand has come at a time when listing inventory is seasonally scarce and has tilted the market from a balanced market back to a seller’s market in many areas. Months of inventory is how we define market conditions. 0-2 months is a seller’s market, 2-4 months a balanced market, and 4 months plus a buyer’s market. In Snohomish County, we ended 2022 with 2.3 months of inventory based on pending sales, and in January 2023 had 1.2 months, and MTD is sitting at 0.9 months. In King County, we ended 2022 with 2.6 months of inventory based on pending sales, and in January 2023 had 1.3 months, and MTD is sitting at 1.1 months.

After months of price reductions and searching for the bottom, we are now starting to come across some multiple offers and price increases. This is leaving clues that the bottom was reached and that we are now stabilizing and looking toward the predicted growth that 2023 has to offer. Buyers are eager for additional selection and will welcome the spring influx of new listings. If sellers are ready, they should not hesitate. Should rates lower as the new listings arrive, sellers will be well supported by a willing buyer audience ready to absorb any growth in inventory.

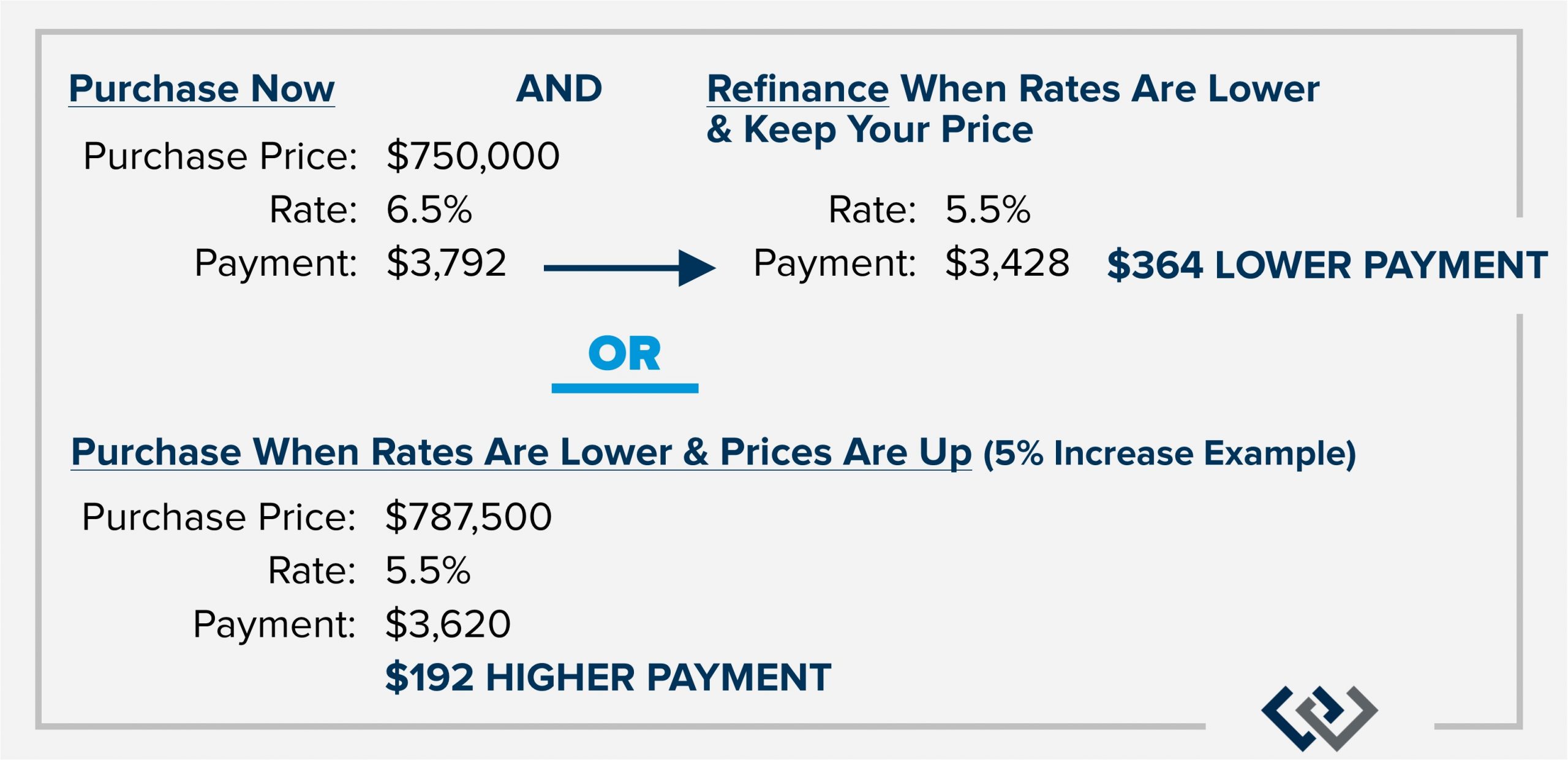

Buyers need to understand that rates and prices are closely related and that waiting for rates to hit a certain point may be detrimental to securing a stabilized price. Many buyers are heading into today’s market with a refinance in mind down the road. They are aware that prices will rise as rates lower, so they are looking to obtain a lower price now with a higher rate and once the rate hits their desired level, they will refinance to lower their payment all while holding on to their lower basis point.

For example, if a buyer bought now at $750,000 with 20% down and a rate of 6.5% their monthly principal and interest payment would be $3,792. If a year from now, rates are at 5.5% and prices are up 5% and that same buyer refinances, they will save $364 a month on their payment and $37,500 in principle. This would also be $192 lower than what the payment would be at the appreciated price with the lower rate!

Real estate moves are driven by life changes. It was completely understandable that many buyers took a pause as the market corrected. Now that the market is showing signs of stabilizing these life changes are pushing buyers to find the home that better fits their lifestyle. Sellers need to keep in mind that their homes need to be priced right and show up to the market well-appointed and properly prepared to get the best results.

We’ve learned a lot over the last year. Once the historical 3-4% interest rate disappeared, consumers had to adapt to the new normal. Now that consumer sentiment is leaning towards a resurgence in demand, opportunity abounds for sellers who are ready to make a move. Please reach out if you are curious about the market trends and want to discuss your goals. It is always my goal to help keep my clients well-informed and empower strong decisions. 2023 is going to be a great year for real estate, I can feel it!

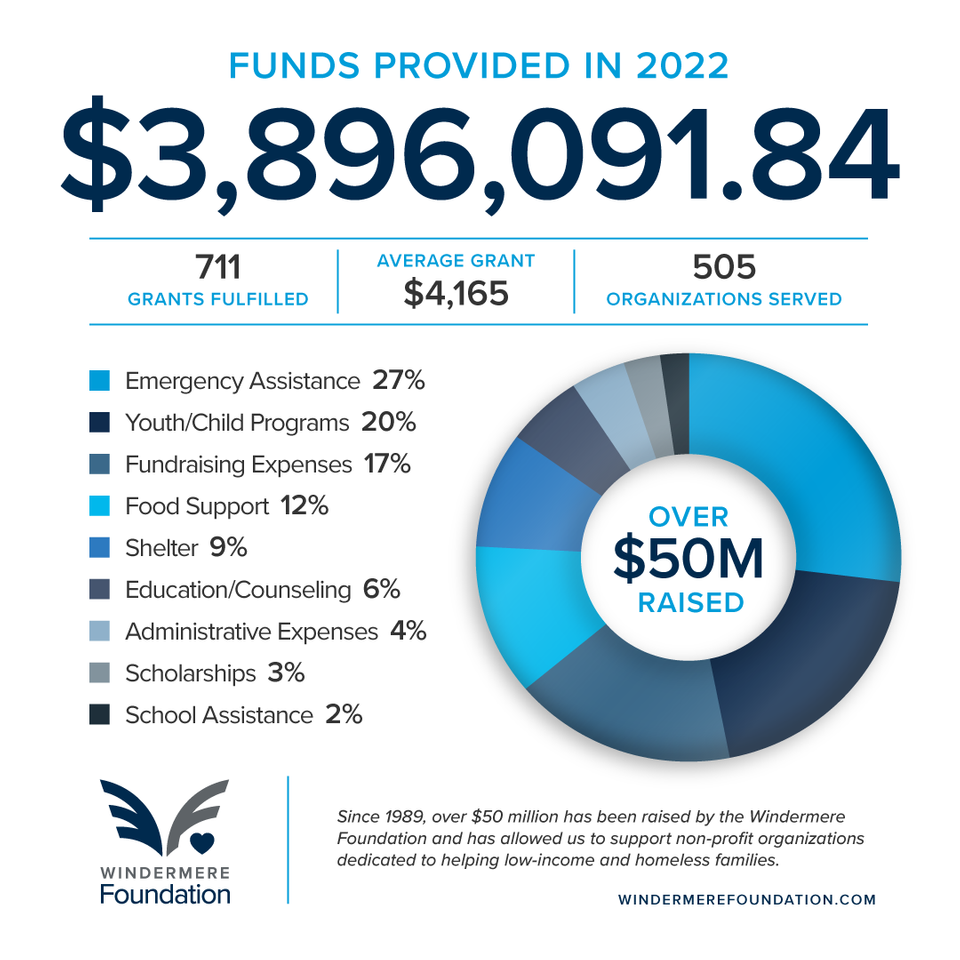

At Windermere we help people buy and sell homes, but we also help build community. I’m proud to support the Windermere Foundation which has raised over $50 million in the past 34 years for low-income and homeless families right here in our local community.

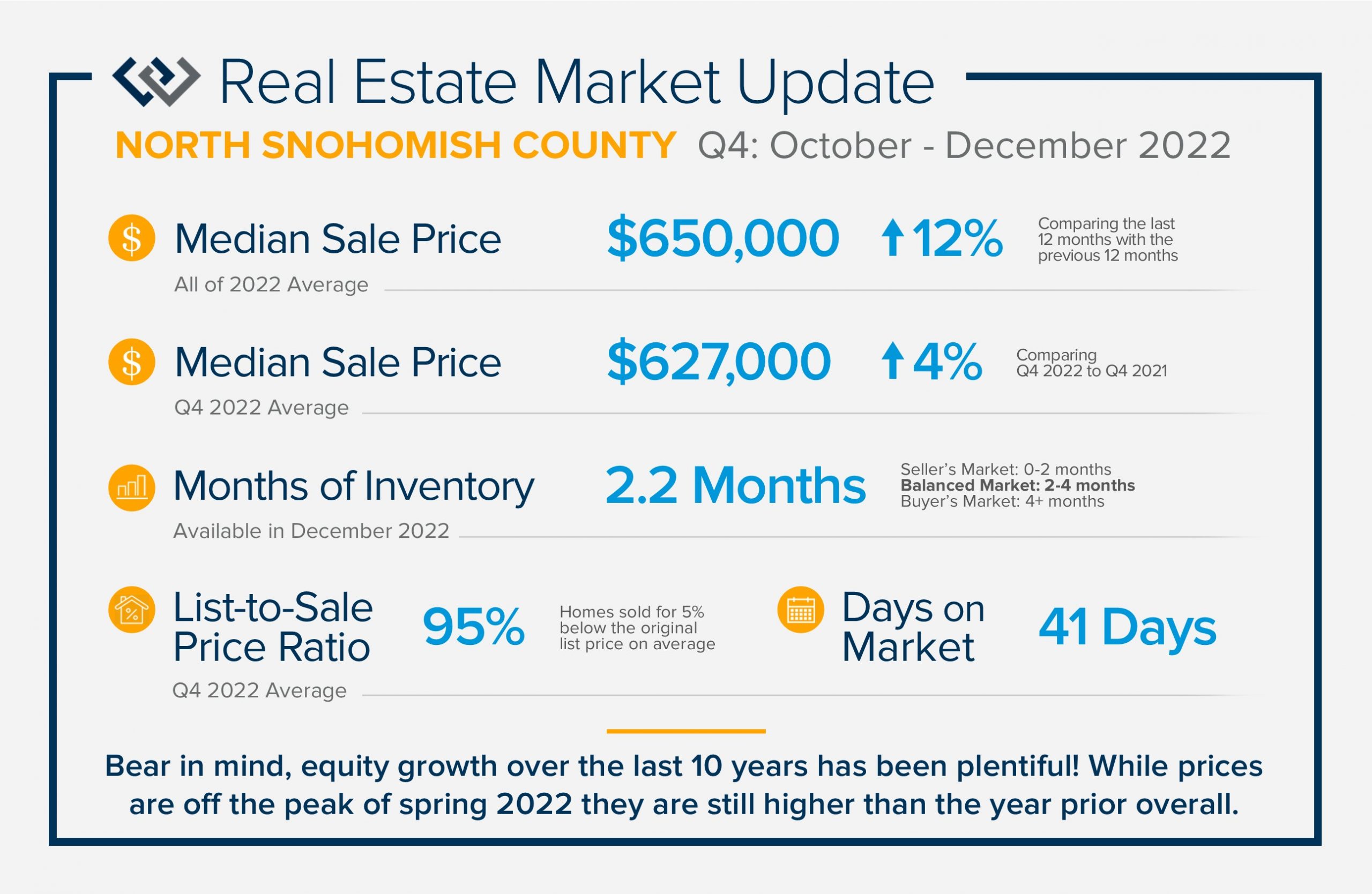

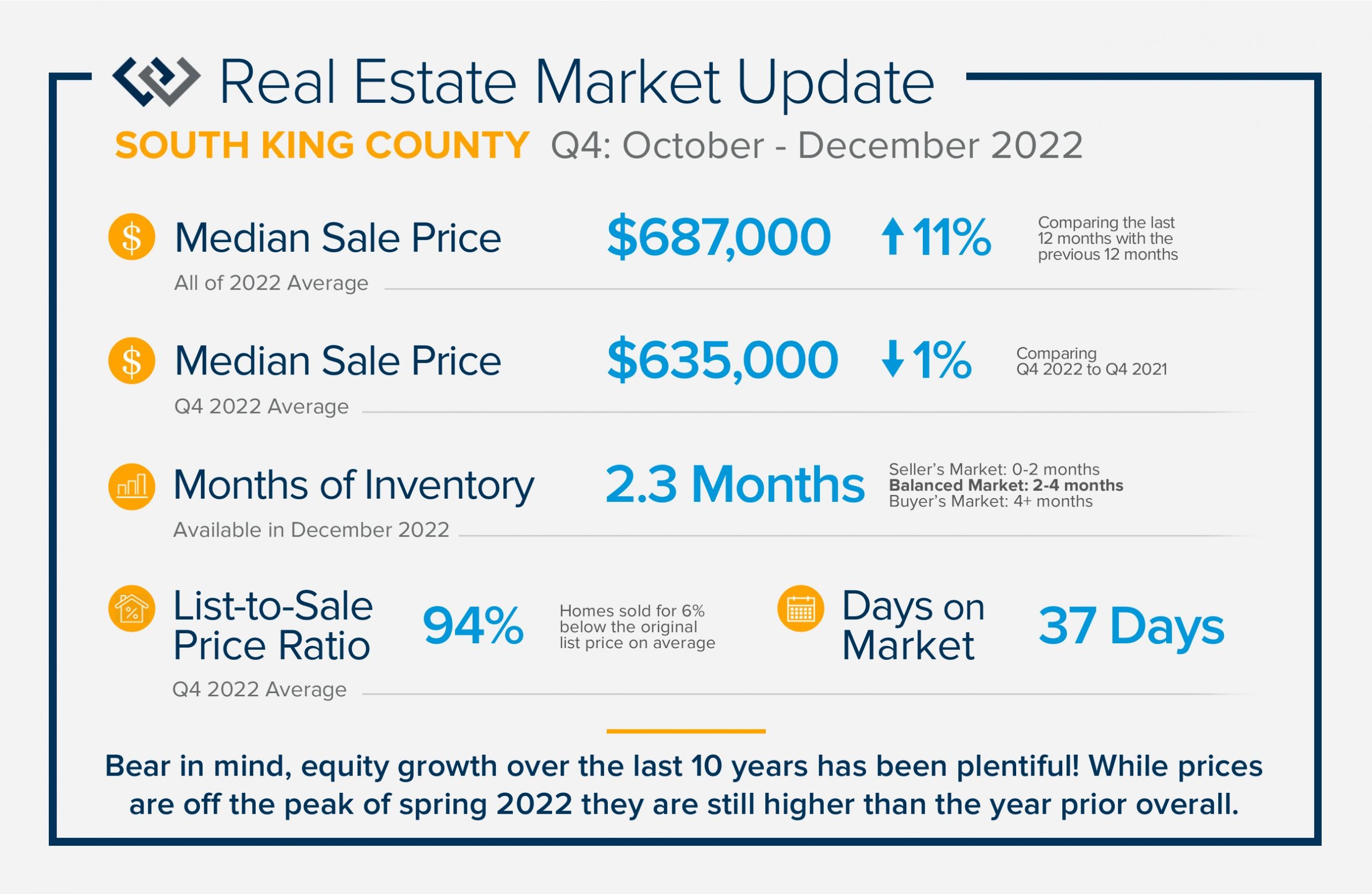

QUARTERLY REPORTS Q4 2022

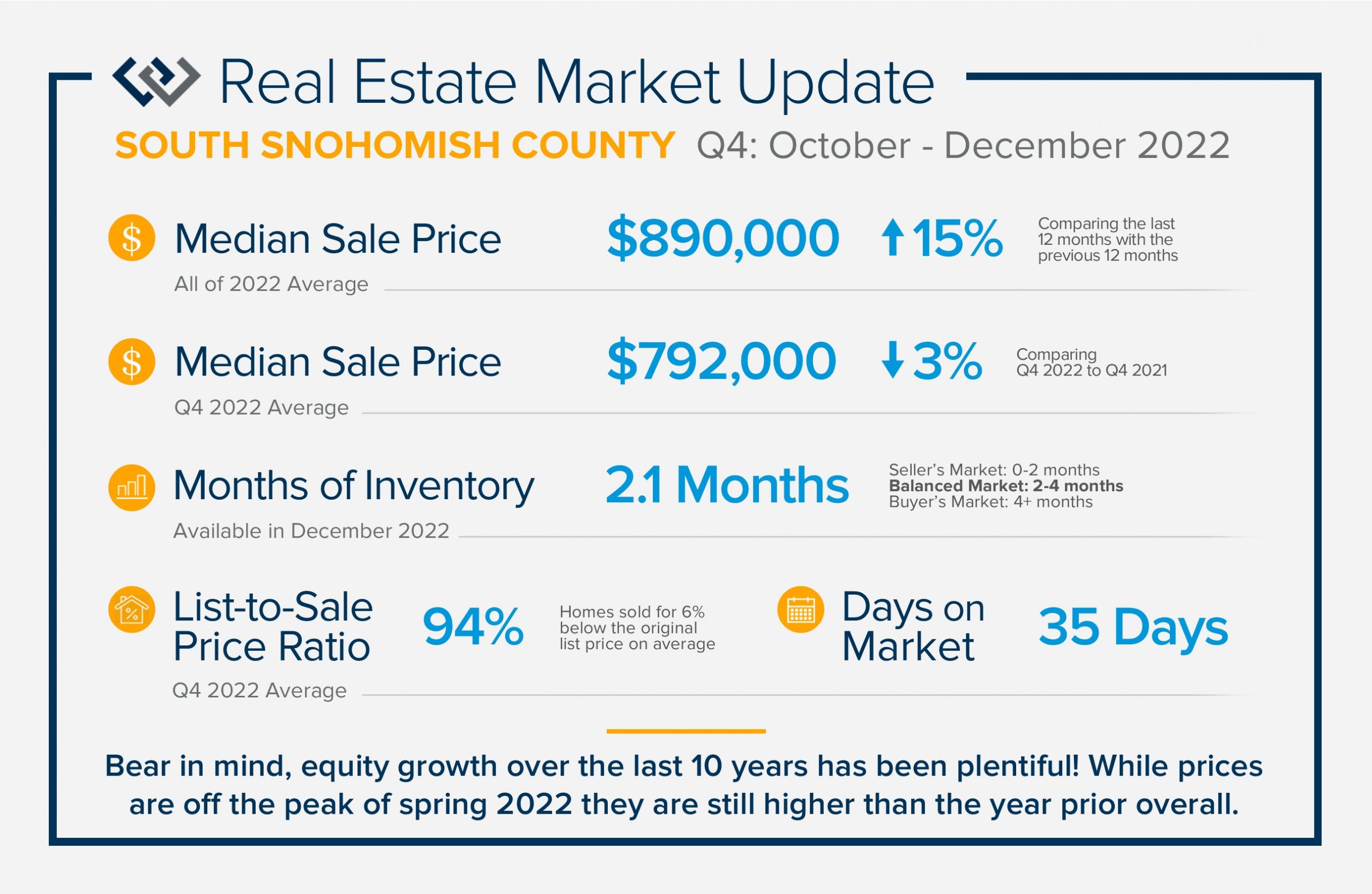

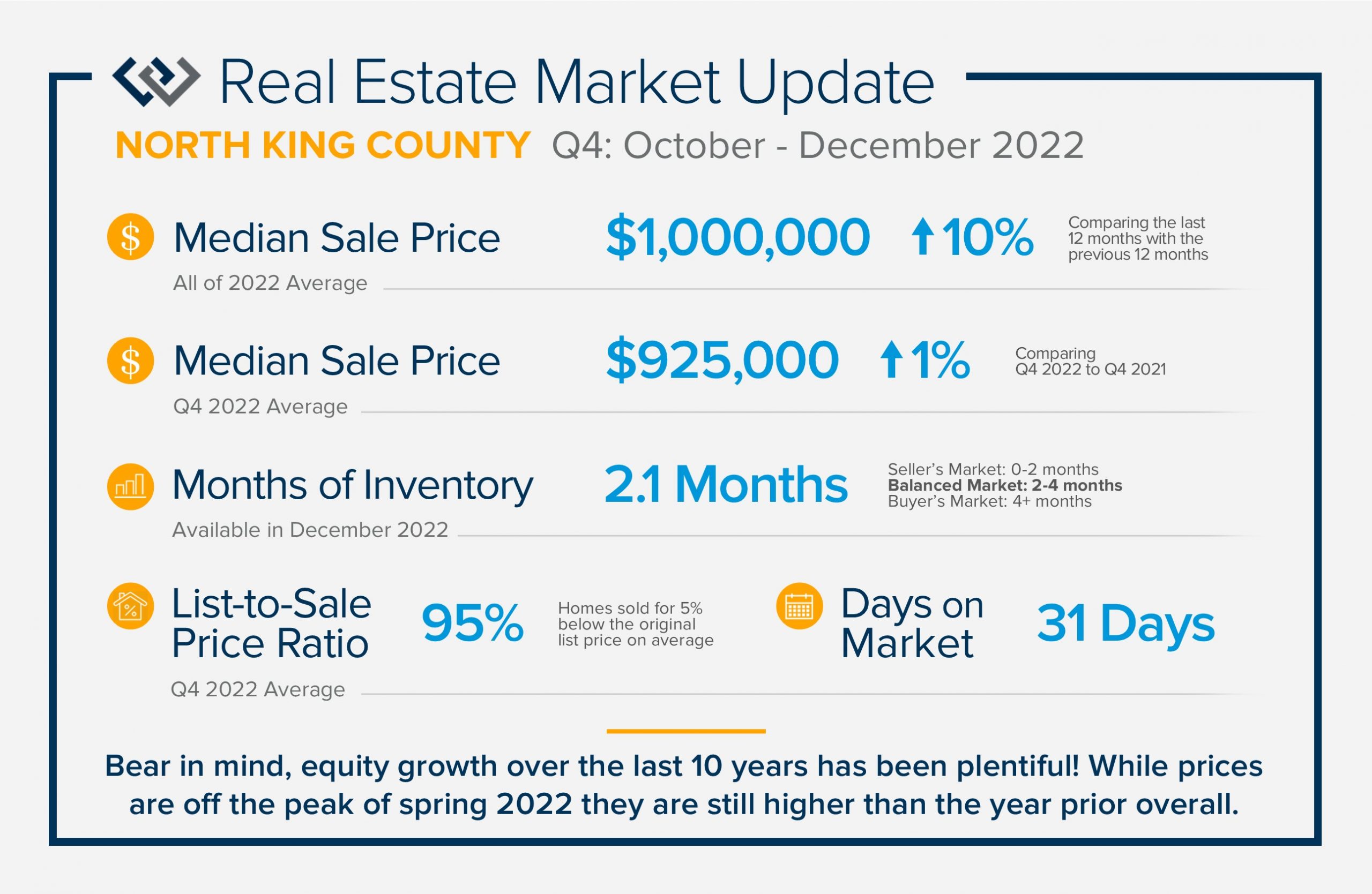

2022 was a transitional year for the real estate market that started off incredibly seller-centric and ended in balance. We started 2022 with interest rates hovering in the low 3%, peaked at 7% in late fall, and ended the year hovering in the mid 6%. This significant jump created a correction in home prices as the cost to finance a home affected affordability. Bear in mind, equity growth over the last 10 years has been plentiful! While prices are off the peak of spring 2022, they are still higher than the year prior overall. 2022 became a more traditional market with interest rates in line with historical averages, more available inventory, and the return of contract contingencies and concessions for buyers. This balance has increased days on market, highlighted the importance of accurate pricing, and made the best-prepared homes shine.

2022 was a transitional year for the real estate market that started off incredibly seller-centric and ended in balance. We started 2022 with interest rates hovering in the low 3%, peaked at 7% in late fall, and ended the year hovering in the mid 6%. This significant jump created a correction in home prices as the cost to finance a home affected affordability. Bear in mind, equity growth over the last 10 years has been plentiful! While prices are off the peak of spring 2022, they are still higher than the year prior overall. 2022 became a more traditional market with interest rates in line with historical averages, more available inventory, and the return of contract contingencies and concessions for buyers. This balance has increased days on market, highlighted the importance of accurate pricing, and made the best-prepared homes shine.

Experts anticipate rates to continue to improve throughout 2023 and buyer demand to grow. Buyers that are looking to enter the market should engage now. Price growth may be flat as we adjust to these norms and then should start to maintain historical annual appreciation rates closer to 2-5% year-over-year after years of double-digit annual growth. If you are curious about how the market affects your housing goals, please reach out. It is my goal to help keep my clients informed and empower strong decisions.

An Economic & Housing Forecast for 2023 by Economist Matthew Gardner

Last week, my office had the pleasure of hosting Windermere’s Chief Economist, Matthew Gardner for his 2023 Economic and Housing Forecast. During this jam-packed hour of insightful delivery, he reported on the U.S. and local economies along with the U.S. and local housing markets specific to King and Snohomish Counties. If you are interested in receiving the recording of the event and/or his PowerPoint slides, please reach out. You can also access the link at the bottom of this newsletter to get his concise forecast for the U.S. housing market.

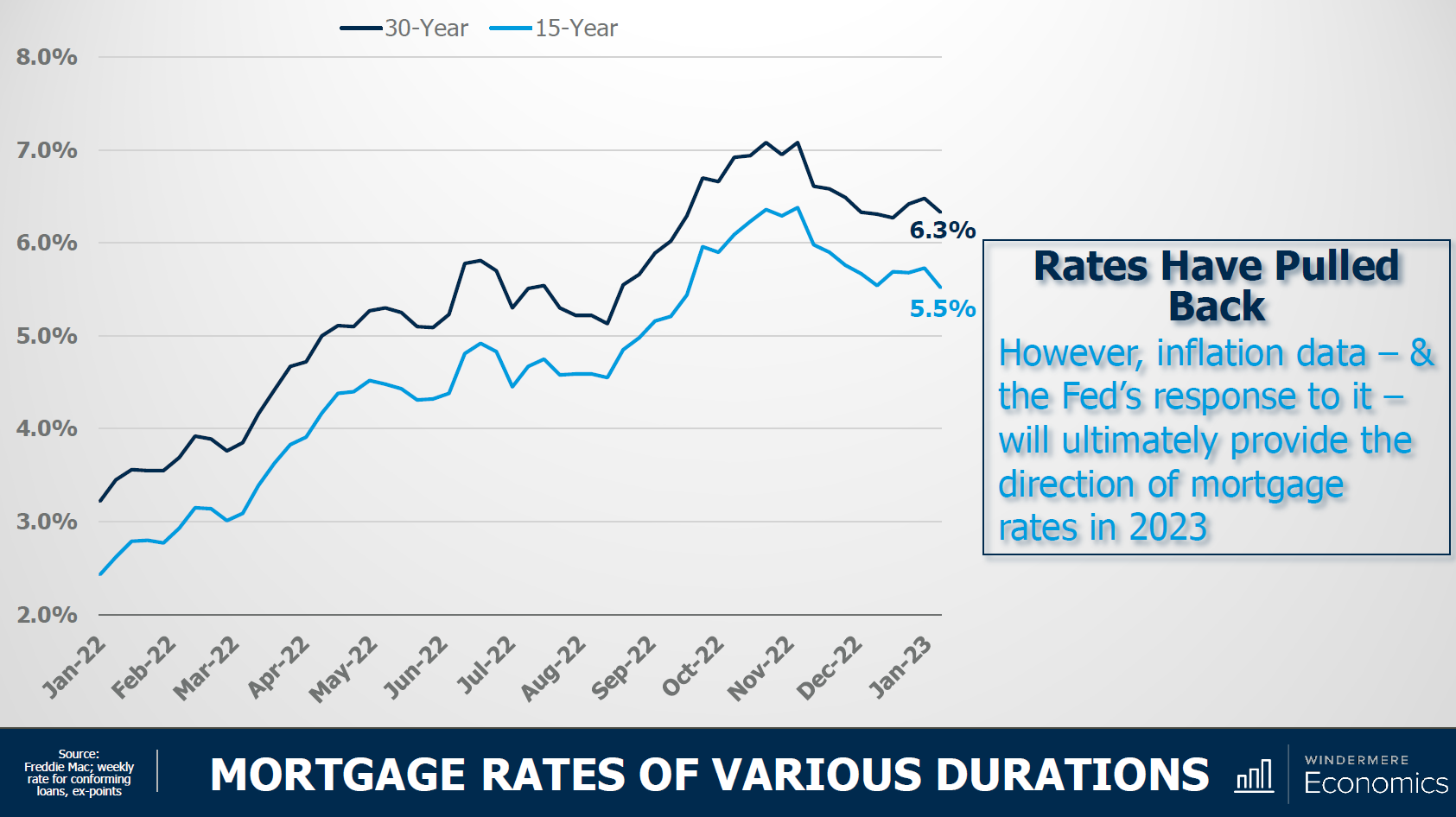

Across the nation, we saw a real estate market correction in 2022 as interest rates doubled. Interest rates started the year at just over 3%, peaked in November at just over 7%, and ended at just under 6.5%. Since the first of the year, we are closer to 6% and anticipate rates to continue to improve towards 5% throughout 2023. The Feds utilized rising interest rates to combat inflation in an effort to create a short recession to slow the cost of all products and services after record-breaking increases during the pandemic. This has reduced spending due to money becoming more expensive to borrow and corrected prices across many industries, including housing.

Across the nation, we saw a real estate market correction in 2022 as interest rates doubled. Interest rates started the year at just over 3%, peaked in November at just over 7%, and ended at just under 6.5%. Since the first of the year, we are closer to 6% and anticipate rates to continue to improve towards 5% throughout 2023. The Feds utilized rising interest rates to combat inflation in an effort to create a short recession to slow the cost of all products and services after record-breaking increases during the pandemic. This has reduced spending due to money becoming more expensive to borrow and corrected prices across many industries, including housing.

The trends across the nation are consistent, but as your local expert, along with the national forecast I am committed to reporting hyper-local facts, figures, and trends to help you understand what is happening and what will happen right in our own backyard. Our local housing market was not immune to the effects of rising interest rates. Our prices peaked in the spring and as rates climbed over 6%, prices took a tumble from the spring highs inflated by cheap money. However, prices are still higher than they were in 2021 which was a recording-breaking year of price growth.

happening and what will happen right in our own backyard. Our local housing market was not immune to the effects of rising interest rates. Our prices peaked in the spring and as rates climbed over 6%, prices took a tumble from the spring highs inflated by cheap money. However, prices are still higher than they were in 2021 which was a recording-breaking year of price growth.

In King County, prices were up 22% in 2021, and in Snohomish County, they were up 23%. We started 2023 with higher prices over 2021, but off the peak of 2022. This is a price reversion, not a housing recession! In fact, in King County, 64% of homeowners with a mortgage have over 50% home equity and in Snohomish County, 63% of homeowners with a mortgage have over 50% home equity. Homeowners are fortified with strong cash positions which is a clear indicator we are nowhere near a housing crisis; we are actually incredibly healthy! While the highs of 2022 were wiped out, the long-term growth we have had over the last decade is the foundation and guiding light of our market. If you bought in 2022, don’t fret, just hold, values will eventually return.

In King County, prices were up 22% in 2021, and in Snohomish County, they were up 23%. We started 2023 with higher prices over 2021, but off the peak of 2022. This is a price reversion, not a housing recession! In fact, in King County, 64% of homeowners with a mortgage have over 50% home equity and in Snohomish County, 63% of homeowners with a mortgage have over 50% home equity. Homeowners are fortified with strong cash positions which is a clear indicator we are nowhere near a housing crisis; we are actually incredibly healthy! While the highs of 2022 were wiped out, the long-term growth we have had over the last decade is the foundation and guiding light of our market. If you bought in 2022, don’t fret, just hold, values will eventually return.

The worst of this correction seems to be behind us as rates are expected to continue to improve throughout 2023 and consumers are adjusting to a more normalized market. Prices are starting to stabilize and are near, if not at the bottom, and should have modest growth in the second half of 2023. We are already starting to see pending sales pick up. Month-to-date (MTD), pending sales are up 25% in King County over December (month-over-month, MOM) and up 21% MOM in Snohomish County. This increase in pending sales is coupled with available inventory being down 15% MOM in King County and down 18% MOM in Snohomish County. Inventory remains tight with MTD inventory levels shifting from a balanced market to a moderate seller’s market based on pending sales rates in both counties.

The worst of this correction seems to be behind us as rates are expected to continue to improve throughout 2023 and consumers are adjusting to a more normalized market. Prices are starting to stabilize and are near, if not at the bottom, and should have modest growth in the second half of 2023. We are already starting to see pending sales pick up. Month-to-date (MTD), pending sales are up 25% in King County over December (month-over-month, MOM) and up 21% MOM in Snohomish County. This increase in pending sales is coupled with available inventory being down 15% MOM in King County and down 18% MOM in Snohomish County. Inventory remains tight with MTD inventory levels shifting from a balanced market to a moderate seller’s market based on pending sales rates in both counties.

It seems that buyer demand is improving and activity is becoming more plentiful. Buyers should take note and be ready to transact if they are poised to make a move. It is a delicate dance between prices and interest rates. Buyers must understand that they can’t change their sale price once they’ve bought, but they can always refinance and change their rate. I have even heard of lenders guaranteeing a future refinance when the rate hits a certain point. Real estate is a long-term hold investment and also where you live. If where you are at doesn’t currently meet your needs, consider a move if you plan to stay there for 5+ years.

Affordability has been a challenge in our area, so if a buyer can obtain a good price this year and then adjust their rate later by refinancing, they will have a much more affordable monthly payment down the road. This takes strategizing and planning and the guidance of a trusted lender and real estate broker. Utilizing adjustable-rate mortgages, rate buydowns, and other creative financing options has put savvy buyers in the catbird seat as they navigate this environment and make exciting moves.

Matthew’s closing words summarized the wild ride of coming off of the pandemic and where we are headed. “2023 will be a transition year when the housing market comes off the high that we saw during the pandemic when borrowing costs were artificially low. I don’t see any reason for buyers or sellers to panic at all! By the end of this year, most markets will have already corrected themselves and we will see prices and demand pick up again, but at a far more normalized pace.”

Real estate is an investment and a lifestyle decision. I am committed to following experts like Matthew and others. I also study the local market trends daily. Markets change quickly and the changes are often reported far after the actual shift. I have understood these shifts due to my daily connection to the market. I take great pride in helping empower my clients to make well-informed decisions about where they live and the financial impact it has on their lives. I love what I do because it is centered in helping people with one of the biggest decisions they will make in their life. If you or someone you know are curious about how the trends relate to your goals, please reach out. I’d be honored to help educate you and help guide and strategize your next move. Here’s to a happy and healthy 2023!

December is for GIVING at Windermere North!

Between holiday parties, family obligations, work, and the pressure of finding the perfect gift, this time of year can come and go in a flash. At Windermere North, we never want this season to go by without coming together to lift up our community and give back in meaningful ways.

Our office-wide annual holiday giving project is in two parts. First, all the brokers in my office joined together to provide $4,242 in grocery gift cards for 16 families, comprised of 48 individuals. Some of these families are dealing with grief and loss this season, some are coming out of domestic violence, some are homeless or unemployed. It is our privilege to partner with Pioneer Human Services for this every year, to help lift some of the burdens for these families.

We also had the joy of helping to bring some holiday cheer for homeless youth in our area. We partnered with WA Kids in Transition who works with social workers in Edmonds School District schools to collect wish lists from homeless students living in shelters, tents, cars, transitional housing or other temporary housing. We fulfilled the wish lists for 14 kids, plus several hygiene kits.

The other Windermere North holiday giving tradition that I love, is volunteering at Christmas House in Everett. Christmas House is a 100% volunteer, non-profit organization that provides an opportunity for qualifying, low-income, Snohomish County parents to select free holiday gifts for their children age infant-18. This is an amazing day helping families in need have a joyful Christmas.

What better way to celebrate Windermere’s 50th anniversary than reaching $50 million in total donations to the Windermere Foundation? Windermere offices across the Western U.S. came together to raise over $4 million this year for low-income and homeless families! Thank you to everyone who helped us get here by giving their time and donating funds. To our clients: a portion of every home sold or purchased goes to the Windermere Foundation, so we couldn’t have done it without you. Here’s to $50 million raised!

Are you curious about the economy during these changing times?

Are you trying to make plans, but crave credible information to assist you?

Please join me for a very special virtual live event:

AN ECONOMIC FORECAST FOR 2023 & BEYOND

with Matthew Gardner, Chief Economist for Windermere Real Estate

Wednesday, January 18, 2023 • 6:30pm – 8pm

Presentation from 6:30-7:30pm, Q&A to follow

Please RSVP by phone/text or email by January 13th, 2023 to receive an emailed link prior to the event.

Key Factors to Note as the Market Recalibrates in the New Year

2022 has been an eventful year in the real estate market and the economy. After 2 years of pandemic-fueled demand and historically low interest rates, we experienced a shift. The Fed quickly raised rates (by 2 points) from April to October to combat inflation, curbing buyer demand as affordability took a hit. The overall economy is starting to settle back to pre-pandemic levels and the second half of 2022 was the time that was needed to make this adjustment.

We have recently seen rates drop as year-over-year inflation numbers start to show improvement. We anticipate this trend to continue slowly but surely as we head into 2023 and beyond. The upward trend in rates has put downward pressure on prices, but they are starting to stabilize as the new normal sets in. Price appreciation is still up year-over-year when you look at the average of the last 12 months and compare them to the previous 12 months, and certainly over the last 3-10 years as a whole.

We started 2022 at 3.5%, peaked at just over 7%, and now find rates in the mid-6%. Experts like Matthew Gardner are anticipating rates to settle in the high 5% sometime in 2023, which would be 2 points below the historical average. Currently, buyers are enjoying more favorable negotiations and are securing sale prices that are not escalating at a feverish pitch.

Some buyers are getting creative and using seller credits for a rate buy-down, some are securing adjustable-rate mortgages, and some just plan to re-finance when rates come down further next year. It is important for buyers to understand that as rates come down prices will start to fortify again.

Besides rates and prices, which are related, two additional factors to pay attention to are our local job market and estimating the recession. We have recently experienced some layoffs in our region, particularly in the tech sector. See the video from Matthew Gardner below which speaks to this. The bottom line is over 20,000 jobs were added in the information sector during the pandemic, and that number is now receding. Just like prices grew exponentially during the pandemic, so did many other aspects of the economy and everything is finding its equilibrium as we return to our new normal. Bear in mind, there are other sectors of our local job market that are growing.

I’d like to leave you with two pieces of advice as we head into 2023 and are forced to jump on the media roller coaster of their reporting economic and real estate news. Pay attention to long-term figures and understand that real estate is a lifestyle move, not just a financial chess move.

The media will paint the picture that the sky is falling and it simply is not. The recession is predicted to be short, much like the recession of 1990-91. Some economists are claiming that we are already through the worst of it. This will be nothing like the Great Recession of 2007-2012, nothing! It just happens to be the one closest in our rear-view mirror and easiest to recall, but that was made up of entirely different factors that do not compare to our current environment. Please reach out if you’d like to further discuss the differences.

We are not headed toward a bubble in the real estate market. Homeowner equity is incredibly strong with over 50% of all homeowners in WA state having over 50% home equity. Homes are not foreclosed on when there is equity—period, end of story. As numbers are reported in the first half of 2023 they will be compared to the peak prices of 2022 and those numbers will create negative headlines. We will spend the first half of 2023 adjusting off of those peaks, but where I am sure the media will fall short is reporting the overall growth in values since 2019.

Real estate is a long-term hold investment, it always has been. The ramp-up of the pandemic years may have clouded that long-term truth, but I can assure you double-digit and certainly 20%+ annual appreciation is not normal. The historical norm is 3-5% annually.

For example, in Snohomish County when you take the last 12 months of median price and average it and compare it to the previous 12 months, prices are up 15%. When you take the median price in Nov 2022 and compare it to the median price in Nov 2021, prices are up 3%. Further, when you take the median price in Nov 2022 and compare it to the median price two years ago in Nov 2020, prices are up 22%. We are experiencing a correction off of the peak, not a tumbling of long-term values. Hence, why there is no bubble.

In fact, experts are anticipating that we end 2023 with positive, yet slight year-over-year appreciation. This is more reflective of historical norms and much calmer than the intense pandemic-fueled years that were inflated with rates that we will quite possibly never see again in our lifetime.

Lastly and most importantly, real estate moves are most often motivated by life changes. Job changes, familial changes, and financial shifts lead to people changing their housing and location. These big life changes are delicate and exciting, and require strategic planning and care. I am all about helping my clients obtain successful financial results, but I am also committed to helping my clients navigate the details, challenges, emotions, and logistics of a move. I always approach the process with the end in mind, but also with the journey prioritized to be smooth and enjoyable.

I hope you call on me when your curiosity is piqued or you have an emergent need in your world related to real estate. I take pride in understanding the latest trends and helping you apply them to your goals. Also, if you know of anyone that needs real estate help, please pass my name along or get me in touch with them. Your people are my people, and helping them stay well-informed to empower strong decisions is my mission. As we encounter change and recalibrate, this expertise will be more important than ever; I am honored to have your trust and endorsement.

Holiday Events = Holiday Giving at Windermere North

We have been busy at our office holding various holiday events that have included the opportunity to give back to the local food banks through holiday food drives. When we bring people together to celebrate it is also a priority to weave in giving back to our community. When we do this, we are always thrilled to partner with Volunteers of America of Snohomish County who support various food banks and food pantries across the county. Just this week, VOA picked up a total of 1,820 pounds of food and $2,480 that resulted from our holiday events.

With inflation still high, food insecurity is prevalent making these food drives an easy choice to direct our giving. If you are looking for a way to give back this holiday season, please reach out to VOA. They are a trusted local organization that will make sure your donation is placed to benefit those in need.

Matthew Gardner’s Top 10 Predictions for 2023

1 There Is No Housing Bubble

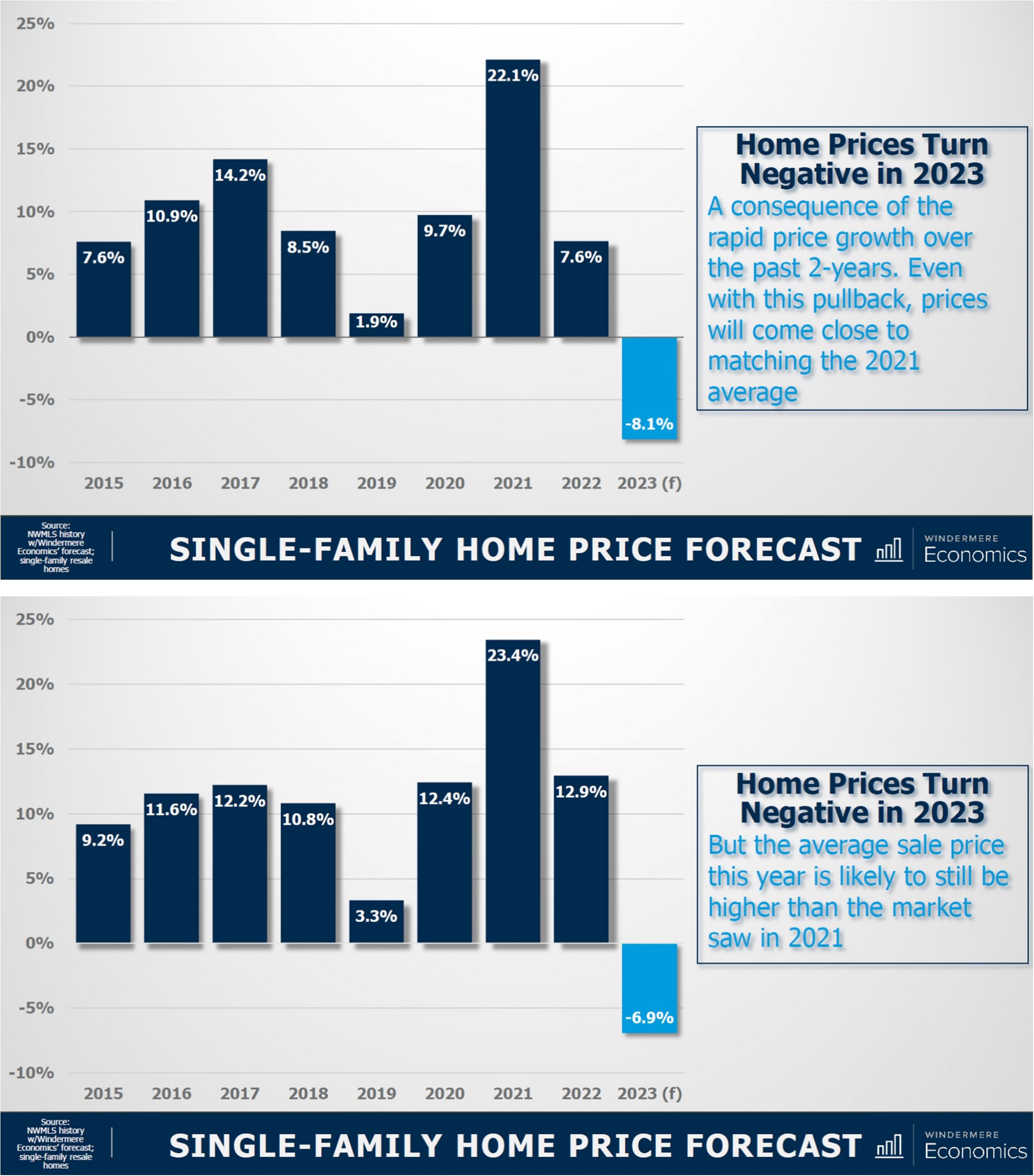

Mortgage rates rose steeply in 2022 which, when coupled with the massive run-up in home prices, has some suggesting that we are recreating the housing bubble of 2007. But that could not be further from the truth.

Over the past couple of years, home prices got ahead of themselves due to a perfect storm of massive pandemic-induced demand and historically low mortgage rates. While I expect year-over-year price declines in 2023, I don’t believe there will be a systemic drop in home values. Furthermore, as financing costs start to pull back in 2023, I expect that will allow prices to resume their long-term average pace of growth.

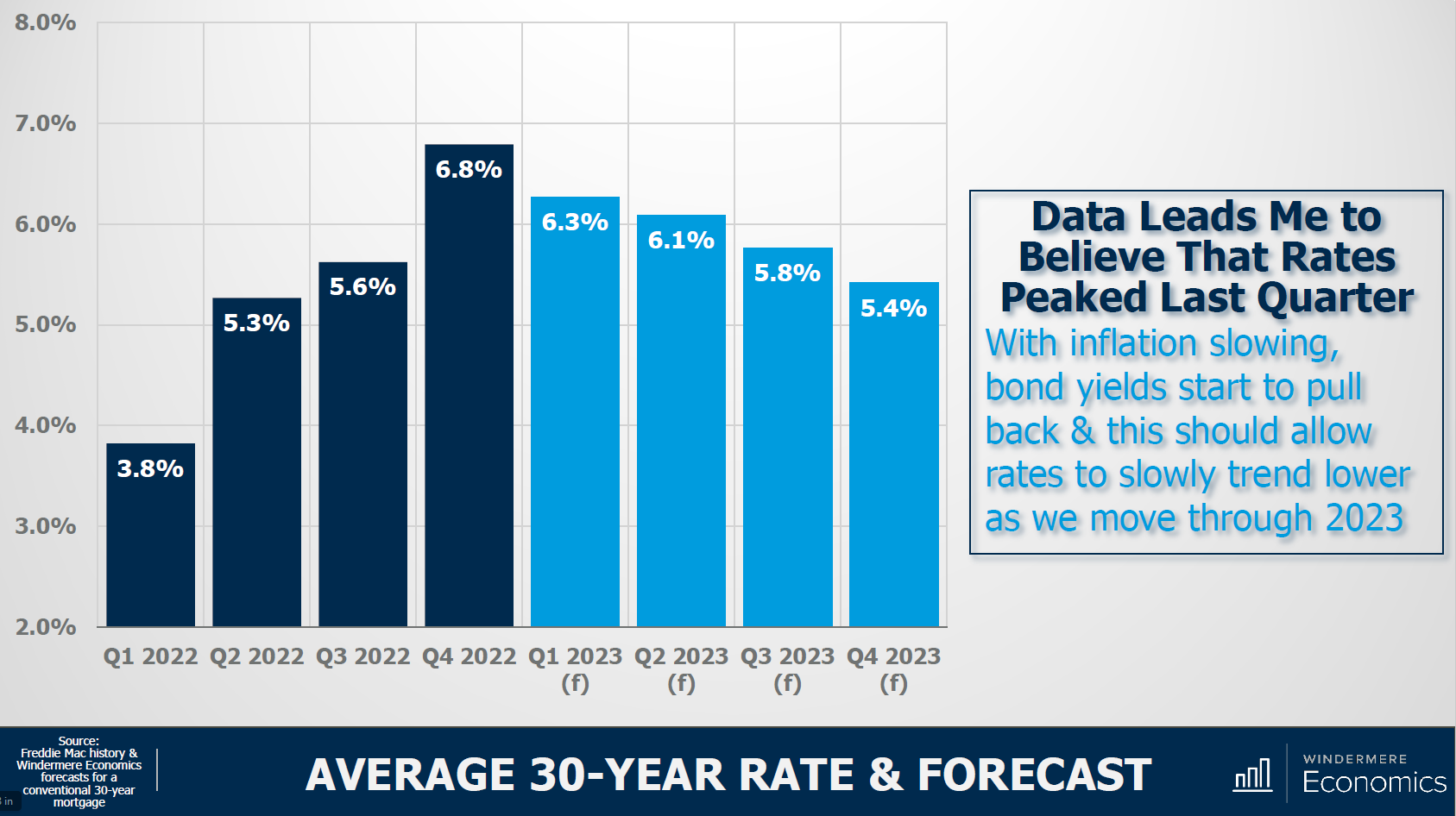

2 Mortgage Rates Will Drop

Mortgage rates started to skyrocket at the start of 2022 as the Federal Reserve announced their intent to address inflation. While the Fed doesn’t control mortgage rates, they can influence them, which we saw with the 30-year rate rising from 3.2% in early 2022 to over 7% by October.

Their efforts so far have yet to significantly reduce inflation, but they have increased the likelihood of a recession in 2023. Therefore, early in the year I expect the Fed to start pulling back from their aggressive policy stance, and this will allow rates to begin slowly stabilizing. Rates will remain above 6% until the fall of 2023 when they should dip into the high 5% range. While this is higher than we have become used to, it’s still more than 2% lower than the historic average.

3 Don’t Expect Inventory to Grow Significantly

Although inventory levels rose in 2022, they are still well below their long-term average. In 2023 I don’t expect a significant increase in the number of homes for sale, as many homeowners do not want to lose their low mortgage rate. In fact, I estimate that 25-30 million homeowners have mortgage rates around 3% or lower.

Of course, homes will be listed for sale for the usual reasons of career changes, death, and divorce, but the 2023 market will not have the normal turnover in housing that we have seen in recent years.

4 No Buyer’s Market But a More Balanced One

With supply levels expected to remain well below normal, it’s unlikely that we will see a buyer’s market in 2023. A buyer’s market is usually defined as having more than six months of available inventory, and the last time we reached that level was in 2012 when we were recovering from the housing bubble. To get to six months of inventory, we would have to reach two million listings, which hasn’t happened since 2015. In addition, monthly sales would have to drop below 325,000, a number we haven’t seen in over a decade. While a buyer’s market in 2023 is unlikely, I do expect a return to a far more balanced one.

5 Sellers Will Have to Become More Realistic

We all know that home sellers have had the upper hand for several years, but those days are behind us. That said, while the market has slowed, there are still buyers out there. The difference now is that higher mortgage rates and lower affordability are limiting how much buyers can pay for a home. Because of this, I expect listing prices to pull back further in the coming year, which will make accurate pricing more important than ever when selling a home.

6 Workers Return to Work (Sort of)

The pandemic’s impact on where many people could work was profound, as it allowed buyers to look further away from their workplaces and into more affordable markets. Many businesses are still determining their long-term work-from-home policies, but in the coming year I expect there will be more clarity for workers. This could be the catalyst for those who have been waiting to buy until they know how often they’re expected to work at the office.

7 New Construction Activity Is Unlikely to Increase

Permits for new home construction are down by over 17% year over year, as are new home starts. I predict that builders will pull back further in 2023, with new starts coming in at a level we haven’t seen since before the pandemic.

Builders will start seeing some easing in the supply chain issues that hit them hard over the past two years, but development costs will still be high. Trying to balance homebuilding costs with what a consumer can pay (given higher mortgage rates) will likely lead builders to slow activity. This will actually support the resale market, as fewer new homes will increase the demand for existing homes.

8 Not All Markets Are Created Equal

Markets where home price growth rose the fastest in recent years are expected to experience a disproportionate swing to the downside. For example, markets in areas that had an influx of remote workers, who flocked to cheaper housing during the pandemic, will likely see prices fall by a greater percentage than other parts of the country. That said, even those markets will start to see prices stabilize by the end of 2023 and resume a more reasonable pace of price growth.

9 Affordability Will Continue to Be a Major Issue

In most markets, home prices will not increase in 2023, but any price drop will not be enough to make housing more affordable. And with mortgage rates remaining higher than they’ve been in over a decade, affordability will continue to be a problem in the coming year, which is a concerning outlook for first-time buyers.

Over the past two years, many renters have had aspirations of buying but the timing wasn’t quite right for them. With both prices and mortgage rates spiraling upward in 2022, it’s likely that many renters are now in a situation where the dream of homeownership has gone. That’s not to say they will never be able to buy a home, just that they may have to wait a lot longer than they had hoped.

10 Government Needs to Take Housing More Seriously

Over the past two years, the market has risen to such an extent that it has priced out millions of potential home buyers. With a wave of demand coming from Millennials and Gen Z, the pace of housing production must increase significantly, but many markets simply don’t have enough land to build on. This is why I expect more cities, counties, and states to start adjusting their land use policies to free up more land for housing.

But it’s not just land supply that can help. Elected officials can assist housing developers by utilizing Tax Increment Financing tools, whereby the government reimburses a private developer as incremental taxes are generated from housing development. There are many tools like this at the government’s disposal to help boost housing supply, and I sincerely hope that they start to take this critical issue more seriously.

As we approach the Thanksgiving holiday, I want to let you know how grateful I am for YOU! Your friendship, support, and referrals have helped fuel my business and support my family. Thank you!

Real estate is a career that gives me the opportunity to be a meaningful part of my clients’ lives as they navigate important moves that have a great financial impact. I take the responsibility of guiding my clients through this process very seriously and know that when someone places this trust in me that it is a big deal! It is an honor to be a part of your big-picture planning and to help you execute these life changes with care and success.

My Thanksgiving would not be complete without taking a moment to say, thank you and that I appreciate you so much! I hope your holiday is filled with happiness, rest, and all the people that are nearest and dearest to your heart.

In honor of Windermere’s 50th anniversary, we’ve set a goal to reach $50 million in total donations to the Windermere Foundation in 2022 for our 50 in 50 campaign. To reach our goal, we need to raise $4 million in donations this year.

So far this year, through the month of October, $3,594,552 in donations has been raised for the Windermere Foundation. If you’d like to help us reach our goal, you can donate here!

Returning to Normal: Buyer Affordability Dictates the Market While Sellers Retain Equity.

There is no doubt that 2022 has been one of the most eventful years in real estate. This is saying a lot coming off the record-breaking years of the pandemic. We will probably never see anything like 2020 and 2021 again. During this time the market responded to a historical event that motivated the rearrangement of our communities due to societal shifts all while we had the lowest interest rates ever. It was a doozy of a time! Demand was spurred by the option to work from home; buyers craved the perfect space to be at home and cheap money made these moves plentiful.

The market had a slight pause at the onset of the pandemic in the spring of 2020 and then it took off like a freight train. Heightened demand, cheap money, and low inventory caused prices to increase at the most significant rate we have ever seen. How was this train barreling down the tracks going to slow down? The speed at which this train was moving was not safe or sustainable. The only way to stop it was an increase in interest rates.

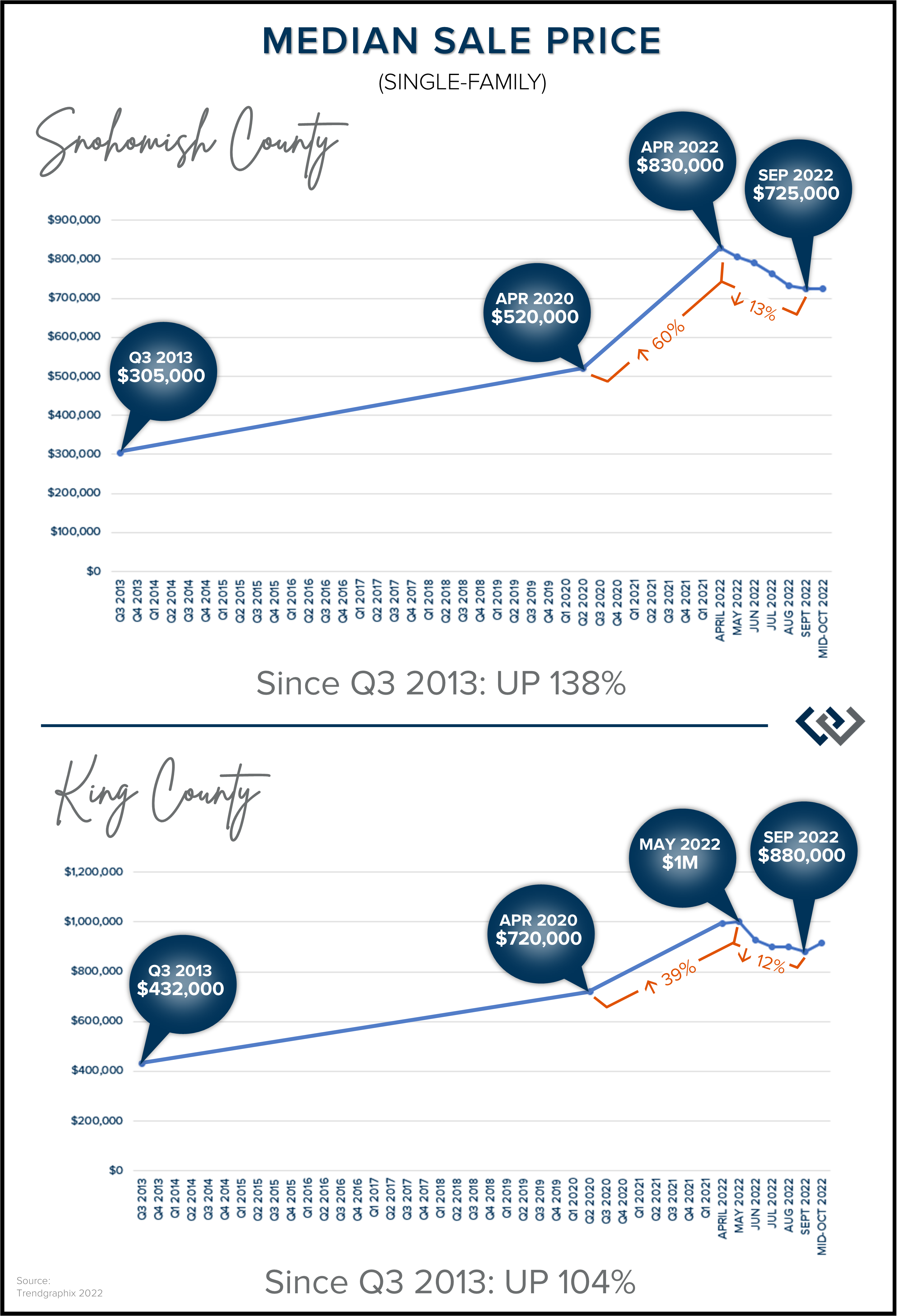

In Snohomish County, from April 2020 to the peak (April 2022) prices grew by 60%, and in King County, from April 2020 to the peak (May 2022) prices grew by 39%. Bear in mind that historical norms for annual price appreciation are 3-5%, making this two-year time period unlike any other! The Fed needed to make the cost of borrowing money more expensive in order to slow down inflation. This was applicable to the entire economy not just real estate, causing short-term rates to increase for credit cards, car loans, and lines of credit, as well as long-term mortgage rates.

In Snohomish County, from April 2020 to the peak (April 2022) prices grew by 60%, and in King County, from April 2020 to the peak (May 2022) prices grew by 39%. Bear in mind that historical norms for annual price appreciation are 3-5%, making this two-year time period unlike any other! The Fed needed to make the cost of borrowing money more expensive in order to slow down inflation. This was applicable to the entire economy not just real estate, causing short-term rates to increase for credit cards, car loans, and lines of credit, as well as long-term mortgage rates.

Since the peak, interest rates have increased by 1.5% and this has put downward pressure on prices and slowed demand. There is a rule of thumb in our industry called the 1/10 rule: for every 1-point change in interest rates, buying power shifts by 10%. For example, if a buyer is pre-approved for a $750,000 purchase at a rate of 5.5% and then the rate increases by 1-point to 6.5% in order for the buyer to have the same monthly payment they must decrease their purchase price by 10% to $675,000. This rule applies when rates go down too, which led to the fierce increase in prices over the pandemic years.

Buyers most often make buying decisions based on the monthly payment and it is no wonder that the new interest rate environment has caused prices to decrease. As you can see from the graph, prices in Snohomish County are down from the peak by 13% and down in King County by 12%, which very much reflects the 1/10 rule, as rates went from 5% on average in April to 6.5% in September. Month-to-date this October, prices in Snohomish County remain even over September prices, and are up slightly in King County.

Expect home prices to adjust based on rate increases, decreases, or stabilization based on the 1/10 rule, not because the sky is falling. Buyers that bought at or around the peak need to keep the faith and understand that real estate is a long-term hold investment with the average homeowner spending at least 8 years in their home. A correction in the market is solved with time and most likely these buyers secured their homes with very low debt service making their payments lower to help them sustain this adjustment. The Fed’s plan is working to slow down the train and help us return to a more sustainable market.

While interest rates are higher than they have been they are still lower than the 30-year average of 7.5% and prices are coming off the peak, but not crashing. In Snohomish County, prices are up 40% from April 2020, and in King County, they are up 22%. Most importantly, long-term price growth since Q3 2013 is up by 138% in Snohomish County and up 104% in King County. In fact, more than 50% of homeowners in WA state have at least 50% equity in their homes making them prepared to make a move when their life-needs will motivate a change. Keeping all of this in perspective will lead sellers to successful moves with a calm understanding of our new normal after an unprecedented time in history.

Buyers are enjoying an increase in selection and more time to make their buying decisions. They now have time to discern these big life changes and to analyze the financial aspect of a move versus needing to make a decision in a 15-minute showing appointment before a home was gobbled up in multiple offers. They are also afforded the opportunity to do further due diligence on the properties they are interested in and negotiate contract contingency terms that protect them throughout the transaction. It is also not uncommon for work orders that a buyer has called out to be added to a contract. We are seeing the occasional multiple offers on homes that are special and priced perfectly, so aligning with a broker who can identify value and opportunity is key so a buyer doesn’t miss out.

Another important aspect for a buyer to consider is the set-up of their financing terms. With rates higher than they have been and the age-old strategy of managing monthly payments always in play, creative financing options such as rate buy-downs and ARMs (Adjustable Rate Mortgages) are additional options to consider when looking at the overall financial picture of making a purchase. Make sure the broker you work with has a collection of reputable lenders that can provide options as each lender will have different programs to choose from.

We are even seeing sellers pay credits on behalf of buyers to buy their rate down in order to make the monthly payment more attainable. The negotiations we are seeing in this market are being dictated by buyer affordability which requires collaboration. Since most sellers have large amounts of equity, we have seen successful meeting-of-the-mind solutions to create win-win outcomes for both sides. As the market comes into balance we are seeing more of a give-and-take and the importance of navigating these changes is critical.

During these times when a market shifts, the cream rises to the top. The listings that are well prepared for the market and priced appropriately will be the winners. Cutting corners and overpricing will lead to frustration and loss. Sellers need to seek out trusted advisors who can properly analyze the new market conditions, bring perspective to their goals, keenly negotiate, and assist them in showcasing their home in the best light possible. Buyers need to align with a professional who understands current market values, can negotiate with data and rapport, assist them in their lending options and help create win-win outcomes.

Brokers like this are not the norm. We are coming off of two years of trying to hold onto a speeding train and now we have the opportunity to steer it through expertise. Expertise is earned and I could not be more passionate about helping my clients navigate the new normal with the tools and experience I bring to the table. I am invested in my clients’ goals and strive to empower strong decisions through thorough research, sound counsel, and clear advocacy. Please reach out if you are curious about how today’s market matches up with your goals or if you know someone I can help.

Did you know Windermere is the official real estate company of the Seahawks?!

The best part of this partnership is our #TackleHomelessness campaign. For every defensive tackle made by the Hawks at their home games throughout the season, The Windermere Foundation donates $100 to Mary’s Place. Our current total is over $200k donated over the last 6 seasons of partnering with the Seahawks.

Since 1999, Mary’s Place has helped thousands of women and families move out of homelessness into more stable situations. Across five emergency family shelters in King County, they keep families together, inside, and safe when they have no place else to go, providing resources, housing and employment services, community, and hope.